Press Release

When Pain Points in Cross-Border Payment Brings Payment Changes, How Can Hypercard Lead the Trend

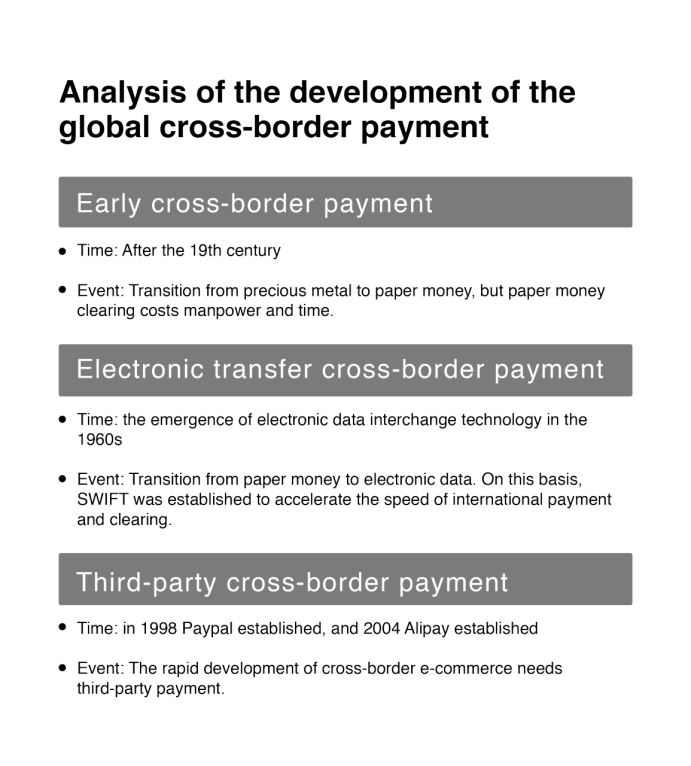

Throughout the evolving history of global cross-border payment, cross-border payment is rising with the continuous development of the international division of labor and international exchanges. In the early days, people use precious metals for cross-border payment and clearing, then followed by paper money, and today’s modern electronic transfer and clearing. Cross-border payment is developing gradually towards a rapid, safe and economical trend as the entire international community is engaging in the activities more frequently and science and technology are changing and progressing.

The change of cross-border payment

According to the data, the total amount of global cross-border payment reached $125 trillion in 2018 and is expected to reach $218 trillion in 2022, promising huge profits.

In the existing transfer and remittance system, the transaction is slow and the cost is high with much margin for error; institutions have to coordinate the value transfer between different internal databases, which makes it extremely difficult to settle transactions quickly. This process not only slows down the transaction progress but also requires large working capital, which has a negative impact on the balance sheet of the institution.

As cryptoassets are gradually accepted by traditional finance, digital currency payment is also implementing and applying quickly. The competition around digital currency has just begun across the globe. In 2019, the emergence of Libra has triggered the catfish effect, and legal currency is discussed more enthusiastically all over the world. Countries have taken precautions and speeded up the research on sovereign digital currency. Even the European Central Bank, which did not seem interested before, recently began to discuss the necessity of developing a unified digital currency. According to a report released by the International Monetary Fund in July of the same year, nearly 70% of the world’s central banks are studying sovereign digital currency.

Some fear that Libra may become a strong currency once in circulation. It can be exchanged with the currencies of countries and erodes the fiat currency. If the weak countries make mistakes in regulation, hyperinflation or even de-monetization will likely happen. In the past, a typical example is Zimbabwe who abolished its local currency and was forced to use the US dollar and other currencies.

Traditional payment giants are fostering digital currency payment

Bitcoin was born to destroy the existing monetary system, which many people think is too expensive and exclusive. Given this, it has a much broader value proposition than a deflationary policy and a hard cap of 21 million coins. The new application of blockchain technology also allows anyone to remit money to counterparties around the world in minutes at a low cost.

This function makes bitcoin directly target the existing payment platforms (such as credit card networks and inter-bank messaging systems). While some companies shrug off these concerns, others see the potential and are looking for ways to create value for partners and shareholders.

According to news on February 20, Visa, an international payment giant, has cooperated with 35 leading digital currency platforms or digital wallets.

These institutions are digital currency platforms licensed by the state or regulated by relevant departments, such as the digital payment platform WireX, the digital currency trading platform Coinbase and Fold, cryptoasset lending platform BlockFi, Austria encryption trading platform Bitpanda, Encrypted debit card platform Crypto.com, etc.

Industry insiders said that the cooperation between Visa and digital currency service providers enables consumers to exchange digital currency more quickly and easily. Users can also deposit this money into their Visa certificates in real-time.

When asked why Visa chose the cryptoasset payment, Visa’s executives clearly expressed their optimism about the payment method in his talks with Forbes: “we saw significant innovation in new financial services for consumers holding digital currency. One example is the growth in demand for digital money lending. We are delighted to work with fintech companies like Cred. The company develops new products in this ecosystem and finds new ways for Visa to improve the entrance of fiat currency associated with these products. “

At present, in addition to Visa, MasterCard, Paypal and other international payment tycoons are also fostering digital currency.

Recently, MasterCard stated that it has cooperated with the Central Bank of The Bahamas to launch the world’s first Bahamas prepaid card. The prepaid card allows people to immediately exchange digital currency into traditional Bahamas dollars and pay for goods and services anywhere MasterCard supports. PayPal also claimed to provide cryptocurrency services to the UK market in the coming months.

Cryptoasset service providers speed up the participation in payment

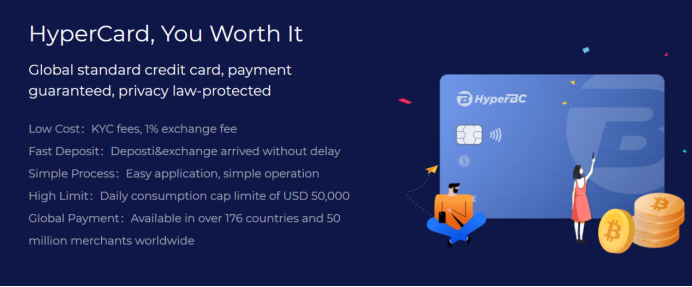

Not only the traditional payment giants are paying attention to cryptoassets payment, but also the asset service providers in the encryption industry are exploring the possibility of payment. HyperBC, a well-known encrypted asset service provider, has launched a comprehensive consumer card HyperCard. After being deposited with digital currency, the card is available in more than 176 countries and more than 50 million merchants worldwide.

As a global standard credit card, HyperCard supports the binding consumption with third-party payment companies by users

Every payment made by HyperCard is secure and consumer privacy is protected by law. HyperCard can transfer money beyond the geographical limit in a second at a low commission, yet with 24/7 service. It is traceable with clear information of all parties. No matter which city you are in, you can use it at all merchants accepting Visa, Master and UnionPay.

In fact, in addition to payment, the most intuitive appealing of digital currency credit cards is it makes encrypted assets purchasing easy and cash out of cryptoassets. In this context, digital currency payment is still a very new track, and the choice of such products is still limited. The main problems are as follows:

1. Only single-currency payment is supported, such as bitcoin

2. Only available in a small number of areas

3. Users have to buy cryptocurrency issued by the card providers before paying

4. Charge a certain percentage of the annual fee

HyperBC also takes this situation into consideration. It is convenient to apply for HyperCard. The digital currency, deposited into HyperCard, can be exchanged into fiat currency in real-time, eliminating the tedious process and the trouble of cash payment, and significantly improving the user-friendliness of digital currency. HyperCard does not charge for KYC verification and only charges a very low commission for each deposit.

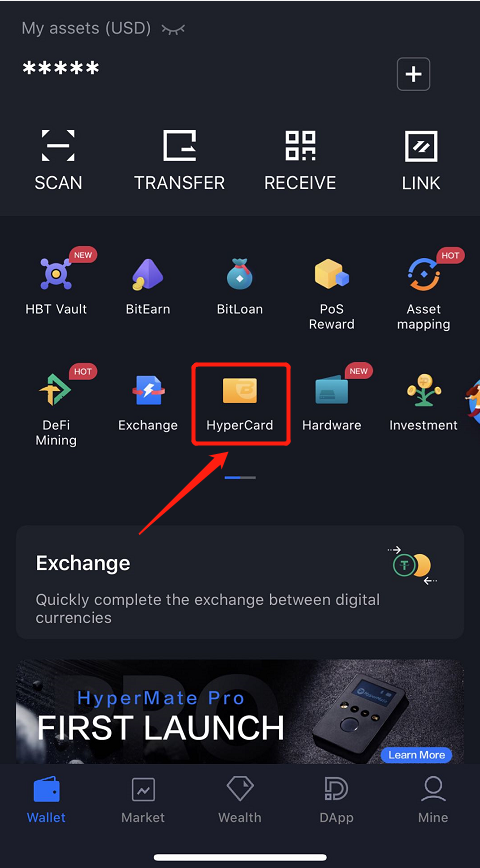

How to apply for HyperCard?

a Download the HyperPay App(https://www.hyperpay.tech/app_down) and register

b Apply for HyperCard

c Submit KYC documents and pass the certification

d HyperCard received

Conclusion

With the rapid development of digital currency and the increasing global acceptance of digital currency, the boundary between fiat currency and digital currency will become narrower. At the same time, digital currency credit card reduces the threshold for traditional users to access digital currency. The selective digital currency assets also avoid their risk in holding digital currency to a certain extent, Whether for investment, quick cash-out, or regular consumption, HyperCard, as a mature digital currency credit card, can enable cardholders to enjoy more convenient services.

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Belarus, 8th Aug 2026 – The case study describes how a participant applied trading education, predefined risk limits, and disciplined decision-making while supporting his family during a period of financial difficulty.

GRODNO, BELARUS – July 14, 2026 – Profit Princess has published a participant case study examining the role of financial education, capital management, and emotional discipline in trading.

The case study follows Mikhail, a 23-year-old resident of Grodno, Belarus, who began studying financial markets while his family was experiencing significant financial pressure. According to Mikhail, accumulated loan interest and overdue payments had placed the family at risk of further collection procedures.

Although Mikhail was employed and contributed to household expenses, his regular income was not sufficient to address the outstanding obligations within a limited period. During this time, he began researching financial market education and discovered content published by Lisa, a trader and analyst associated with the Profit Princess community.

The educational materials focused on market fundamentals, trading discipline, capital preservation, risk control, and common mistakes made by inexperienced market participants. The content did not present trading as a guaranteed or immediate source of income.

After reviewing the available materials, Mikhail enrolled in the Traderclass by Liza educational program. The program is designed to introduce participants to trading principles, including market analysis, position sizing, loss limits, capital management, and the psychological factors that may affect decision-making.

Education Before Market Participation

Before allocating personal funds, Mikhail completed the educational program and observed trading sessions conducted through the Profit Princess community.

His initial trading capital was USD 1,000, which he had accumulated before joining the program. According to the case study, Mikhail established several rules before beginning to trade. These included limiting the amount of capital used in individual positions, defining potential losses in advance, recording trading results, and stopping activity after reaching a predetermined daily loss limit.

The case study states that Mikhail experienced both profitable and unprofitable trades during the initial period. Rather than increasing position sizes after losses, he reviewed his decisions and continued studying the educational materials.

Mikhail also participated in community trading sessions where market situations and completed trades were analyzed. The purpose of these sessions was to help participants understand the reasoning behind trading decisions rather than encourage the automatic replication of individual positions.

According to Mikhail, maintaining discipline was particularly difficult because of the financial pressure affecting his family.

“When a family is dealing with debt, there is a strong temptation to make decisions quickly and take additional risks. The main principle emphasized during the training was to protect capital before focusing on potential profit,” Mikhail said.

Application of Predefined Risk Limits

During the four-week period described in the case study, Mikhail continued working at his regular job and traded during his available time.

Before each trading session, he established a maximum acceptable risk and a loss level at which he would stop trading. He also maintained records of his entries, exits, results, and reasons for making each decision.

The case study reports that this process helped Mikhail reduce impulsive decisions and identify recurring mistakes. It also allowed him to evaluate his activity based on adherence to a system rather than the result of a single trade.

Profit Princess emphasizes that risk management cannot eliminate the possibility of financial loss. Trading performance may be affected by market volatility, execution conditions, participant experience, emotional decisions, and other factors.

Reported Result After Four Weeks

According to account information provided for the case study, Mikhail’s trading balance increased from USD 1,000 to USD 5,500 over four weeks. The reported difference of USD 4,500 represented trading profit before considering any personal tax obligations that may apply.

Mikhail subsequently withdrew USD 3,500 and transferred the funds to his parents. The remaining trading balance was USD 2,000, consisting of his original capital and USD 1,000 in reported profit.

According to the participant, the withdrawn funds allowed the family to reduce its overdue balance and continue discussions regarding a revised repayment schedule. The payment did not eliminate all of the family’s financial obligations, but it provided additional time to address the remaining balance.

“The result was important because it gave the family an opportunity to stabilize the situation. It did not remove the need for continued work, careful budgeting, and further payments,” Mikhail said.

Focus on Process Rather Than Individual Returns

Profit Princess states that the case study is being published to demonstrate the importance of preparation, predefined limits, and emotional control. The company does not present Mikhail’s reported performance as typical or reproducible.

Lisa noted that individual financial results should not be separated from the time spent studying, reviewing mistakes, documenting decisions, and avoiding trades that did not meet established criteria.

“The final account balance is only one part of the case study. The more relevant element is the participant’s ability to follow predefined rules despite significant emotional pressure. Trading education should focus on responsible decision-making and risk awareness, not on promises of rapid income,” Lisa said.

Mikhail continues to work at his regular job and participate in financial market education. According to the case study, he does not currently plan to increase his trading volume substantially and remains focused on maintaining defined risk limits.

He also does not describe himself as a professional trader. His stated priorities are continuing his education, supporting his family, and avoiding decisions based on urgency or emotion.

Risk Disclosure

Trading in financial markets involves a substantial risk of loss and may not be suitable for every person. Participants may lose some or all of the capital allocated to trading.

The performance described in this case study represents the reported experience of one participant during a specific period. It should not be interpreted as a guarantee, forecast, investment recommendation, financial advice, or indication of future results.

Market conditions and individual outcomes vary. Anyone considering participation in financial markets should independently assess the risks, review applicable legal and tax requirements, and seek advice from a qualified financial professional where appropriate.

Media Contact

Organization: Profit Princess

Contact Person: Victoria Hayes

Website: https://t.me/+DwU5IXGj6ONmZTEy

Email: Send Email

Country:Belarus

Release id:47985

The post Profit Princess Publishes Trading Education Case Study Focused on Risk Management appeared first on King Newswire. This content is provided by a third-party source.. King Newswire makes no warranties or representations in connection with it. King Newswire is a press release distribution agency and does not endorse or verify the claims made in this release. If you have any complaints or copyright concerns related to this article, please contact the company listed in the ‘Media Contact’ section

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Quatre Bornes, Mauritius, August 08, 2026, ZEX PR WIRE — CapitalXtend has announced the launch of its refreshed identity and redesigned website, marking an important milestone in the company’s continued evolution. The update reflects CapitalXtend’s commitment to creating a more modern, accessible, and client-focused trading experience while strengthening the foundation for its next phase of growth.

This represents more than a visual update. It reflects CapitalXtend’s ongoing investment in improving how traders engage with the company across every touchpoint. Alongside the new identity, the redesigned website introduces a cleaner interface, improved navigation, and a more intuitive structure, making it easier for both new and existing clients to explore the company’s products, platforms, and trading services.

The enhanced digital experience enables traders to access account information, compare trading solutions, explore platform features, and navigate market opportunities with greater ease. Every improvement has been designed to simplify the user journey while maintaining the professional standards, reliability, and performance for which CapitalXtend is known.

This milestone also reinforces CapitalXtend’s broader commitment to innovation and continuous improvement. By refining its digital experience and strengthening the way traders interact with the brand, CapitalXtend continues to invest in making its services more accessible, intuitive, and user-focused. As part of its offering, traders continue to benefit from solutions such as CFD Shares, Holders Account, Return on Equity, and Unlimited Leverage.

Existing clients will experience a seamless transition, with no changes to account credentials, funds, or account types. The updated platform allows traders to continue operating without interruption while benefiting from a more refined digital environment.

Speaking on the milestone, Dr. Farrukh Adeeb, Group CEO & Chairman of XGroup, said:

“This is an important milestone for CapitalXtend. Our refreshed identity reflects how the company has evolved and where we are heading next. Beyond a new look, this launch represents our continued investment in delivering a better experience for our clients, making it simpler to access our services, navigate our platform, and trade with confidence as we continue to grow.”

The website is now live, representing another step in the company’s journey to deliver a trusted, innovative, and client-centric trading experience for its global community.

About CapitalXtend

CapitalXtend is a global multi-asset broker committed to delivering a secure, transparent, and technology-driven trading experience. Offering access to a wide range of financial markets through advanced trading platforms, the company continues to focus on innovation, client-centric service, and empowering traders with reliable trading solutions.

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Press Release

Grepix Infotech Highlights White Label Apps as a Smart Business Model for On-Demand Entrepreneurs

Grepix Infotech shares industry insights on how enterprise-grade white label technology is helping entrepreneurs launch faster, reduce technology costs, and compete in the growing on-demand economy.

Noida, Uttar Pradesh, India, 8th Aug 2026 — Grepix Infotech Pvt Ltd, a globally recognised on demand technology company powering app businesses across 30+ countries, today published its industry perspective on the question every technology entrepreneur eventually faces: do you build your own platform from scratch, or do you launch faster and smarter using a proven white label solution?

For entrepreneurs targeting the on demand economy in 2026 — one of the fastest-growing and most competitive commercial landscapes in the world — the answer has never been clearer.

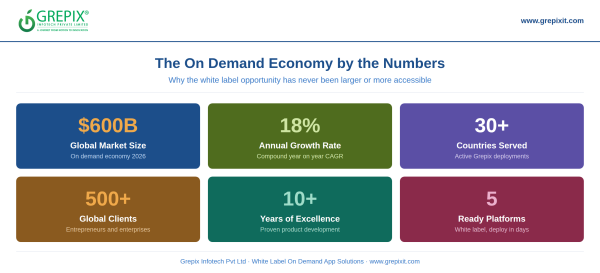

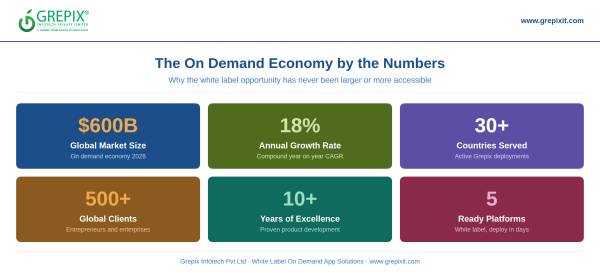

A $600 Billion Market With No Room for Slow Movers

The global on-demand economy is now valued at over USD 600 billion and growing at a compound annual growth rate of over 18 percent. From ride-hailing giants like Uber, Bolt, and Didi to food delivery leaders like DoorDash, Glovo, and Jumia Food, the playbook has been written. Consumers in every market — from São Paulo to Kuala Lumpur, Karachi to Cairo, and Manila to Mexico City — have already formed on-demand habits. They expect instant service, real-time tracking, and seamless digital payments as a baseline — not a luxury.

The opportunity for regional entrepreneurs is enormous. The platforms dominating global headlines are not winning in every city, every town, or every emerging market corridor. There are thousands of underserved markets across Asia, Africa, Latin America, Eastern Europe, and the Middle East where a fast-moving, locally operated on-demand business can capture significant market share — if it gets there fast enough.

That is exactly where white label technology changes the game entirely.

Why Most On-Demand Startups Never Make It to Launch

Across hundreds of client engagements spanning markets from Dhaka to Dubai, Bogotá to Bangkok, and Accra to Auckland, Grepix has observed a consistent and sobering pattern: the most common reason on-demand startups fail is not a flawed business model or insufficient funding. It is the time, cost, and complexity of building the technology itself.

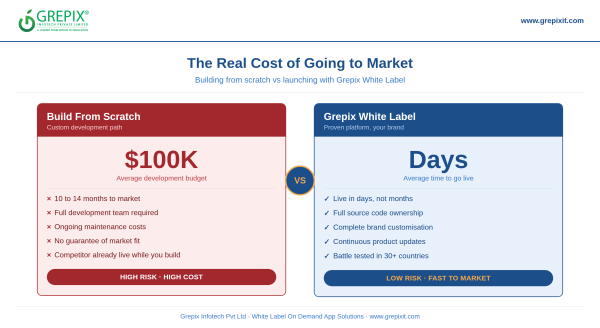

Building a competitive ride-hailing platform — with a passenger app, driver app, admin panel, real-time GPS dispatch, dynamic surge pricing, and multi-gateway payment integration — requires a minimum development timeline of 10 to 14 months and a budget typically ranging between USD 40,000 and USD 100,000, depending on team quality and feature scope. That figure excludes ongoing maintenance, server infrastructure, security updates, and the continuous feature development required to stay competitive in a rapidly evolving market.

By the time a custom-built app launches, a competitor running on a proven white label platform has already acquired drivers, signed up restaurants, onboarded service providers, and locked in early customer loyalty.

“We have seen brilliant entrepreneurs with the right market insight, the right capital, and the right team — completely derailed by a development cycle that consumed 18 months and twice their planned budget. By launch day, someone else already owned the market,” said a spokesperson for Grepix Infotech. “The technology timeline does not just slow a business down. It can kill it entirely.”

What Modern White Label Actually Delivers

The white label model of 2026 bears no resemblance to the generic, off-the-shelf software of a decade ago. Today’s enterprise-grade white label platforms like those built by Grepix offer full source code ownership, complete brand identity customisation, region-specific feature configuration, dedicated technical onboarding, and continuous product updates informed by real-world deployments across diverse global markets.

Entrepreneurs who choose white label do not receive a template. They receive a battle-tested, commercially proven technology foundation that has already processed millions of transactions, resolved thousands of edge cases, and been refined across deployments in markets as diverse as Saudi Arabia, Brazil, Vietnam, Ghana, Turkey, and Colombia.

A white label deployment through Grepix can be live in under two weeks at a fraction of the cost of custom development with zero compromise on quality, scalability, or brand identity.

Speed to Market is the Real Competitive Moat

In the on-demand economy, first-mover advantage is not a cliché. It is a commercial reality.

The platform that signs up drivers first, the aggregator that onboards restaurants before anyone else, and the logistics operator that locks in enterprise clients early — these businesses build supply and demand flywheels that are expensive and time-consuming for any competitor to replicate. Just as Bolt disrupted Uber across multiple markets by moving fast and operating with local agility, and just as Grab built a dominant super app position across Southeast Asia by prioritising speed of market penetration over perfection of technology, regional entrepreneurs can carve out dominant positions in their own cities and countries — if they launch before the window closes.

White label eliminates the development delay entirely. Rather than spending a year building, entrepreneurs can redirect every dollar and every hour into driver acquisition, restaurant partnerships, hyperlocal marketing, and customer experience — the activities that actually determine whether an on-demand business survives and scales.

Five Verticals Where White Label Delivers the Strongest ROI

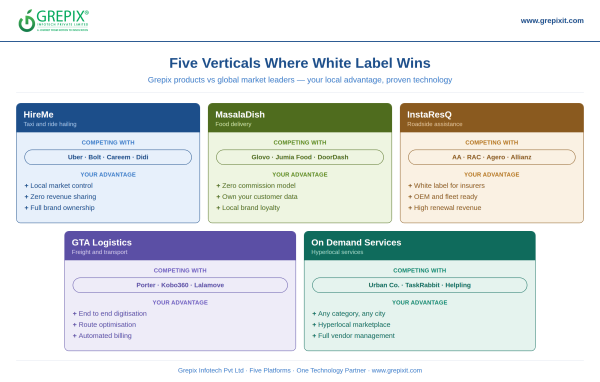

Ride Hailing and Taxi — Where Uber, Bolt, and Careem dominate at a global scale, hundreds of city-level and country-level markets across Indonesia, Morocco, Kazakhstan, Peru, and Senegal remain open to locally operated alternatives. Grepix’s HireMe taxi app platform gives entrepreneurs a fully branded, Uber-class ride-hailing business with intelligent dispatch, surge pricing, and real-time GPS tracking — deployable in days, not months.

Food Delivery — As Glovo, Jumia Food, Talabat, and DoorDash expand across markets from Istanbul to Lagos and from Riyadh to Ho Chi Minh City, the demand for locally owned and zero commission alternatives is accelerating rapidly. Grepix’s MasalaDish food delivery platform lets entrepreneurs launch a fully independent food delivery business — retaining complete control of margins, customer data, and vendor relationships in a way the large aggregators will never offer.

Roadside Assistance — A high renewal, high retention vertical with strong demand from insurance companies, automobile manufacturers, and fleet operators across markets including the UAE, South Africa, Malaysia, Argentina, and Egypt. Grepix’s InstaResQ Roadside Assistance platform connects stranded drivers to the nearest verified service provider in minutes — white labeled and fully brandable for any insurer, OEM, or fleet operator entering this space.

Logistics and Freight — As platforms like Porter, Kobo360, Lalamove, and Trukker have demonstrated across India, Nigeria, Hong Kong, and the UAE, digitising freight logistics is a multi-billion-dollar opportunity in every emerging and developing market on the planet. Grepix’s GTA Logistics platform gives logistics entrepreneurs a complete digital freight operation — booking, real-time fleet tracking, route optimisation, proof of delivery, and automated billing — without a single line of custom code, ready to compete from day one.

Home and Hyperlocal Services — In markets where Urban Company, TaskRabbit, Helpling, and Handyman have proven the hyperlocal services model across India, the United States, Germany, and the United Kingdom, the opportunity for locally operated equivalents across Thailand, Nigeria, Chile, Jordan, and the Philippines remains wide open and largely uncontested. Grepix’s On Demand Services platform enables entrepreneurs to launch a fully configured hyperlocal marketplace across any home service category — cleaning, beauty, appliance repair, healthcare — in virtually any city, in virtually any market, within days.

White Label Is Not a Shortcut — It Is a Growth Strategy

The most successful franchise and platform businesses in the world — from global fast food networks to logistics giants — do not build proprietary technology stacks from the ground up. They adopt proven operational systems, focus investment on local execution, and compete on customer relationships and market knowledge.

White label on-demand technology follows exactly the same principle. The entrepreneurs winning in the on-demand space in 2026 are not the best developers. They are the best operators — and white label gives them the technology infrastructure to operate at full commercial scale from week one, in any city, in any country, with any brand name they choose.

For any entrepreneur evaluating entry into the on-demand economy, the question is no longer whether white label is credible or capable enough. The question is whether they can afford the capital burn, the time delay, and the competitive risk of not using it.

About Grepix Infotech Pvt Ltd

Grepix Infotech Pvt Ltd is a New Delhi-based technology company and the developer behind HireMe, MasalaDish, InstaResQ, GTA Logistics, and the Grepix On Demand Services Platform. With 500+ clients across 30+ countries and over a decade of product development experience, Grepix is the white label technology partner of choice for entrepreneurs and enterprises building on-demand businesses across Africa, the Middle East, South Asia, Southeast Asia, and Latin America.

Media Contact

Organization: Grepix Infotech Pvt. Ltd.

Contact Person: Vinay Jain

Website: https://www.grepixit.com

Email: Send Email

Contact Number: +918860213347

Address:Logix Technova A 328, Noida-Greater Noida Expy, Block B, Sector 132, Noida, India – 201304

City: Noida

State: Uttar Pradesh

Country:India

Release id:47948

The post Grepix Infotech Highlights White Label Apps as a Smart Business Model for On-Demand Entrepreneurs appeared first on King Newswire. This content is provided by a third-party source.. King Newswire makes no warranties or representations in connection with it. King Newswire is a press release distribution agency and does not endorse or verify the claims made in this release. If you have any complaints or copyright concerns related to this article, please contact the company listed in the ‘Media Contact’ section

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Profit Princess Publishes Trading Education Case Study Focused on Risk Management

CapitalXtend Launches New Brand Identity and Enhanced Digital Experience

Grepix Infotech Highlights White Label Apps as a Smart Business Model for On-Demand Entrepreneurs

Benzinga Money Article Discusses How to Become Part of the 12% of Retirees Who Have Achieved the Recommended $550,000 Minimum Retirement Savings Threshold

Apu Apustaja Conquers New York with Lively Street Ads, Including Times Square Billboard

Bay Smokes Maintains Quality Amid Legislative Changes in the Hemp Industry

-

Press Release2 days ago

STARTRADER in Discussions with Trustpilot to Consolidate Review Profiles

-

Press Release1 week ago

ISGroup Publishes Large-Scale Study Showing AI Can Identify Real Software Vulnerabilities

-

Press Release1 week ago

The Future of Preventative Healthcare! Dr. Sundardas Annamalay and Dr. Narjit Singh’s Newly Released Book Sheds Light on Cellular Health

-

Press Release1 week ago

Shattering Industry Norms: Don Kilam Drives Global Expansion Backed by $35.8M Portfolio

-

Press Release1 week ago

D$AVAGE Releases New Hit Single “Chosen One”

-

Press Release1 week ago

TaqFlow Emerges to Overhaul Central Asian Cross-Border Payments

-

Press Release1 week ago

The Growing Demand for Sober Lifestyle Products Reflects a Changing Culture

-

Press Release1 week ago

The Church of Conceptual Art Opens Ticketing for the Afterlife