Press Release

In-depth analysis report-IPFS and Filecoin

Intro:

The current situation of Filecoin is not optimistic as negative news emerges frequently. Can IPFS really be implemented on a large scale? Whether multiple futures products on the market can solve the current situation of Filecoin? And what kind of role can IPFS play in the future? This article will provide an in-depth analysis from a third-party perspective.

On October 15th, with the launch of mainnet, Filecoin finally opened its final chapter after preparing for three years. However, IPFS did not meet people’s expectations, and even various negative events happened one after another. What is the future of Filecoin?

Why IPFS was born?

To trace the origin of Filecoin, we must start with IPFS. The birth of IPFS is closely related to the current status of the Internet.

Internet technology has three basics elements: computing power, storage, and bandwidth, especially in the storage sector. Information storage can be said to be the foundation of the entire Internet. The storage methods HTTP used by the traditional Internet underlying protocol are centralized. That is to say, the traditional Internet needs to establish a centralized storage node first, and then connect all the terminals in the network through the HTTP protocol, and on this basis, to serve various applications in the Internet.

In general, centralized storage has three disadvantages:

First, the storage and transmission efficiency is low;

Second, the data security has serious problems;

Third, the storage cost is high.

In response to the shortcomings of these centralized storage, in 2014, Juan Benet, a computer doctor of Stanford University, innovatively proposed a concept of distributed storage to optimize the Internet system.

In May 2014, Juan Benet launched the IPFS Interplanetary File System, and got a huge investment in the YCombinator incubation competition in 2015, and finally established the development team Protocol Labs to build the IPFS system.

IPFS is essentially an underlying Internet protocol for hard-disk sharing. It is a storage network that allows people to share their idle storage space and obtain revenue.

The files stored in the IPFS network are broken up into several 256 kb file fragments through a special encryption algorithm, and then these file fragments are scattered and stored on the servers of miners around the world. When users need data, they only need to input instructions, and the nearest nodes that store the same data will transmit data to users at the same time.

IPFS can effectively reduce the possibility of high concurrency while greatly improving the efficiency of data transmission. The emergence of IPFS is indeed a revolution in Internet storage. Here’s an analogy: if all vehicles are driving on the same road, it is very likely to cause traffic congestion or paralysis. If there are multiple roads to choose from when the vehicle departs, the probability of congestion will be much reduced.

The working principle of IPFS is to divide the data into parts and store them in different nodes. What each node gets is not all of the data, but a 256kb file fragment. Therefore, the distributed storage method of IPFS can also effectively avoid security issues such as natural disasters, hacker attacks, and data leakage. At the same time, compared with HTTP, IPFS greatly saves bandwidth resources and reduces data redundancy. So this is why IPFS is so popular in the world and it is so important.

The application situation of IPFS

Based on its decentralized characteristics, IPFS received huge financial investments at the beginning of the project, including Bole YCombinator, Sequoia Capital, Winklevoss Brothers, Digital Currency Group, Stanford University, Anderson Horowitz Fund, FC Emerging Network Equity Crowdfunding Institution, Union Square Ventures USV etc., with a total financing of more than 257 million US dollars. However, these investments are to obtain equity in the parent company, and Filecoin did not give the investors any token commitments. It was not until August this year that IPFS Labs compromised and promised to give these shareholders in the form of tokens.

IPFS, which is born with gold, is also fully blooming in terms of real market applications. First, let’s look at the application of search engines.

Firefox product manager Mike Conca published an article on Mozilla’s official website stating that Firefox’s browser extension applications support distributed protocols including IPFS, that is, supporting for the “ipfs://” protocol.

Google Chrome is also adding a plug-in IPFS Companion to the extended application to help users better run and manage their own nodes locally, and view the resource information of IPFS nodes at any time.

Opera browser has cooperated with IPFS for a long time. Its Android version of Opera browser has launched IPFS support and developed crypto wallet in the browser with Android, iOS and desktop versions.

In addition to the three major engine browsers, there are also IPSE and Poseidon search engines. These two search engines are both search engines based on the IPFS network and mainly serve for blockchain projects.

The second is file transfer applications. IPFS already has some application carriers, including Partyshare, Pinata and IPWB. For example, Partyshare is an open source file sharing application built on the peer-to-peer hypermedia protocol IPFS, which allows users to share files using IPFS.

In community and e-commerce applications, applications like Indorse, Steepshot, Peepeth, Origin, Open Bazaar, etc. have also appeared. All of the above applications use the IPFS protocol.

On the whole, although the total number of IPFS related applications has reached nearly one hundred, the application of IPFS on the three mainstream engines is only in the form of a plug-in, and file transfer is only to improve the storage needs of IPFS. Peripheral applications are also on some related blockchain platforms, and there is no large-scale implementation.

IPFS tries to move towards a path of full coverage in the blockchain application industry. Compared with the reports that the media claimed that IPFS will replace HTTP and subvert the entire Internet when IPFS was first born, IPFS has not been possible to complete that goal in recent years or more than a decade. The most prominent ability of IPFS is its decentralized storage capacity in a specific range. Blockchain is only a portrayal of database technology. For a behemoth like HTTP, IPFS currently does not have any practical application capabilities to shake it. IPFS still has a long way to go.

The incentive layer Filecoin

The association between Filecoin and IPFS is simple. Filecoin is the incentive layer on the IPFS protocol. To put it another way: IPFS is not a blockchain, nor a certain token, but an Internet protocol. Filecoin is the IPFS protocol token, a payment transaction token for distributed storage nodes under the IPFS protocol. Its purpose is to reflect the financial value of IPFS in the form of tokens for market circulation and transactions.

Filecoin’s blocks run on a new type of proof mechanism called “space-time proof”, and will be mined by miners who store data. The Filecoin protocol does not rely on a network consisting of a single coordinated and independent storage provider to provide data storage and retrieval services, among which:

(1) The user pays tokens for data storage and retrieval,

(2) Storage miners earn tokens by providing storage space,

(3) Search miners to provide data services to earn tokens.

Filecoin turns cloud storage into an algorithmic market. This algorithm market is based on a local protocol, Filecoin (FIL), where miners can obtain by providing storage to customers.

In turn, customers spend Filecoin to obtain storage space.

Filecoin was questioned when it went online

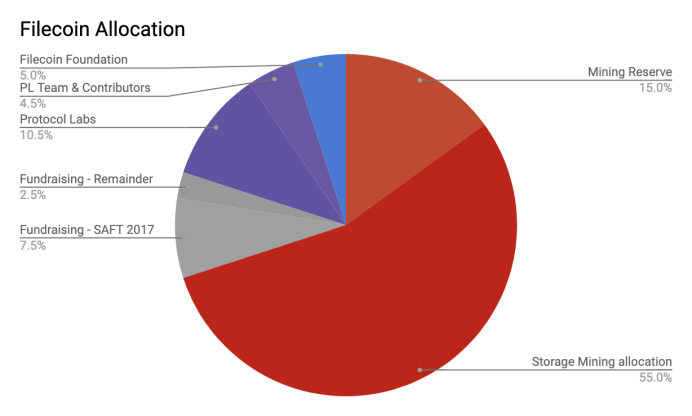

Filecoin token distribution rules are as follows:

The total upper limit of Filecoin is 2 billion, called FIL_BASE. In the distribution of Filecoin’s genesis block, 30% is allocated to financing, Protocol Labs and Filecoin Foundation. among them:

10% of FIL_BASE is allocated to financing institutions, 7.5% of this 10% is sold, and the remaining 2.5% will be used for ecological development, follow-up financing and other purposes.

15% of FIL_BASE is allocated to the protocol laboratory (including 4.5% to the laboratory team and contributors), and the final 5% is allocated to the Filecoin Foundation.

The remaining 70% is allocated to Filecoin miners as mining rewards for providing data storage services, maintaining blockchain, distributing data, running contracts, etc.

Over time, these rewards will support multiple types of mining, so this section will be broken down to cover different types of mining activities. The following is all the distribution rules of Filecoin tokens.

At 22:44 pm on October 15, 2020, Filecoin mainnet was finally officially launched. During the space race, miners were able to mine at a maximum rate of 1PB per day. On the second day of the mainnet launch, the leading miners collectively protested the strike and stopped increasing their computing power. Behind this was the helplessness of the miners.

On the morning of October 18th, less than three days after the launch of Filecoin mainnet, Filecoin official sensed the tremendous pressure from miners. Filecoin core staff Molly posted on Slack that the FIP-0004 proposal has been received by the community, and the content of the proposal will be applied when Filecoin network is updated next week, that is, 25% of storage miner block rewards will be released directly, and the other 75% will still be linearly released at 180 days.

On the morning of October 21st, Filecoin official momack2 posted the latest news on the slack channel saying: “The Lotus 1.1.0 version will be launched. The biggest highlight of this version is the FIP-4 proposal that has been passed a few days ago. The passage of the proposal means that 25% of the block rewards for storage miners can be released immediately.”

Many miners and crypto investors did not approve of this official move. The official retreat may be able to solve the current market problems, but the changes in the rules and models have made many people feel the crisis of trust in Filecoin. The biggest feature of the blockchain is the trust mechanism. Even if the good news is based on the change of the mechanism model, it is difficult to convince miners. After all, while some people benefit, some people will suffer losses.

The number of miners is not as expected and the market is bleak

Let’s look at the market participation status of Filecoin. In addition to Filecoin’s trust crisis in China market, PANEWS found in a Filecoin-related questionnaire survey conducted by worldwide investors that foreign users are not very interested in Filecoin.

PANEWS interviewed 22 interviewees in total, most of whom have more than three years of experience in the crypto circle. Of the 22 respondents, 19 respondents have heard of Filecoin, accounting for 86%. Only 22.7% knew about Filecoin and IPFS, and only 13.6% had participated in Filecoin mining or purchased FIL tokens and futures.

Among them, many interviewees claimed: They are not optimistic about Filecoin, and the it is more like a hype. Compared with participating in Filecoin’s ecology, people are more willing to use Filecoin to make quick money. In addition, some investors also believe that: Filecoin should not allow miners to bear mining pressure and legal risks at the same time.

In addition, there are some professionals who are not optimistic about IPFS, claiming that the underlying protocol of IPFS is still not comparable to existing cloud storage solutions such as Dropbox, iCloud, and Google, let alone to challenge and replace them.

More facts prove that Chinese miners account for 80% of Filecoin miners. Juan also stated it on Twitter: Thousands of miners around the world are using Filecoin. The vast majority are Chinese miners. In the FILFOX browser, almost all of the top ten mining nodes are from China.

Filecoin conspiracy theory

This wave of disputes among miners has not yet settled, and Filecoin’s price performance in the secondary market has also plunged. The data website shows that the current price of FIL is 24.3 US dollars, which is too far away from the expectation that the price of around 200 US dollars when it was launched.

Within a few days of the mainnet just being launched, 1.5 million FIL tokens were transferred from an unknown address, and 800,000 FIL was transferred to Huobi Exchange. According to Filecoin’s unlocking plan, early investors, officials and miners should unlock only 500,000 coins on the first day. With the official promise that FIL tokens will not be sold in the early days, where do these tokens come from?

In response, Filecoin team gave an official response, calling this unknown account an official account. The transfer of these FIL tokens is mainly to ensure market stability. The tokens are bought and sold on exchanges to provide market liquidity, stabilize price, and correct imbalanced incentives for miners. The transfer of these tokens is not a FIL sale by Protocol Labs. The market-making plan is for the benefit of the community to ensure that there is liquidity in the market at the beginning and maintain price.

On October 20th, another 30,000 FIL were transferred from an unknown address. As of the date of publication, the official team has transferred 909,000 FIL. If calculating on the basis of the price of FIL at 170 dollars when it was launched, the total value is more than 150 million dollars. Even if at the current market price which is 20 dollars, the value of these FIL is more than 20 million dollars.

Large amount of FIL flew into the market, and small investors are the biggest losers in the secondary market. The plunge in the price of FIL has a lot to do with the fact that the test coin can be bought and sold as the mainnet coin. According to Filecoin’s official statement before, all sectors in the space race zone 1 and 2 will be migrated to the main network, and the pledge of these sectors and the block rewards obtained will also be migrated to the mainnet. The encapsulated effective computing power, pledged FIL and mined FIL test coins will be migrated to the mainnet in a certain proportion.

However, after the mainnet went live, the flow of test coins was directly transferred to exchanges for trading, which also allowed the miners who dominated the space race to gain a lot of FIL. While those who hold FIL are rejoicing in absenteeism, it is a disaster for those who do not own FIL and the small investors in the secondary market.

In response to this incident, Filecoin official members explained that the test coin can be directly used as the mainnet coin is a special design, not a “bug”. This is to ensure the security of the network. The miners sold tens of millions of FIL immediately after the mainnet went live, which was “seriously exaggerated”, and the actual amount sold was only 1/10 to 1/100 of the number mentioned in the report. Regardless of the amount of data, it is undeniable that the selling behavior of these miners is one of the factors that contributed to the plunge in FIL price. And from the official explanation, it is obvious that it is to provide shelter for these absenteeism, and the so-called absenteeism is very likely to be an official black-box operation.

The reputation and price of FIL have both encountered Waterloo. Juan Benet sent dozens of Twitter to refute rumors and respond, but the fact that Filecoin is going down cannot be concealed. The only incentive layer, Filecoin, is in a deep development dilemma and it is difficult to survive. This makes the future path of trying to subvert the entire Internet application layer protocol standard IPFS again full of variables.

QFIL and FIL futures products

Back to the secondary trading market, FIL price plunged. Excluding mining income, FIL’s acquisition channels are more important in the early stage from exchanges. Before FIL is officially launched, FIL’s futures products have been the highlight.

Let’s take a look first, what are the futures products in the market?

FIL6: 6-month FIL futures products, with the same redemption period, which is 180 liner release period as the same as mining rules;

FIL12: 12-month FIL futures product;

FIL36: 36-month FIL futures product.

Based on the popularity of Filecoin, many exchanges have launched FIL futures in the early stage.

Among them, the QFIL product launched by QuickCash (QC issuer) and first released on the ZB.com platform has been popular by many users. Because QFIL supports redemption within 15-30 days after FIL goes online, it is faster than many 6-month/12-month futures. In addition, QFIL is an ERC20 token and supports DeFi mining. At present, ZB.com has also supported depositing QFIL to QC (1:1 stablecoin anchored to offshore CNY), and the price of QFIL, which supports multiple game modes, has surpassed FIL once.

Conclusion

Futures products like QFIL can solve the liquidity problem of FIL to a certain extent and also inject new market momentum into the development of FIL.

As far as the status quo of Filecoin is concerned, the future of Filecoin requires the efforts of various aspects. Filecoin bears the expectations of too many investors, but blindly pursuing investment returns will only destroy it. Only by continuously improving its own mechanism and strengthening its application can IPFS go further and further.

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Belarus, 8th Aug 2026 – The case study describes how a participant applied trading education, predefined risk limits, and disciplined decision-making while supporting his family during a period of financial difficulty.

GRODNO, BELARUS – July 14, 2026 – Profit Princess has published a participant case study examining the role of financial education, capital management, and emotional discipline in trading.

The case study follows Mikhail, a 23-year-old resident of Grodno, Belarus, who began studying financial markets while his family was experiencing significant financial pressure. According to Mikhail, accumulated loan interest and overdue payments had placed the family at risk of further collection procedures.

Although Mikhail was employed and contributed to household expenses, his regular income was not sufficient to address the outstanding obligations within a limited period. During this time, he began researching financial market education and discovered content published by Lisa, a trader and analyst associated with the Profit Princess community.

The educational materials focused on market fundamentals, trading discipline, capital preservation, risk control, and common mistakes made by inexperienced market participants. The content did not present trading as a guaranteed or immediate source of income.

After reviewing the available materials, Mikhail enrolled in the Traderclass by Liza educational program. The program is designed to introduce participants to trading principles, including market analysis, position sizing, loss limits, capital management, and the psychological factors that may affect decision-making.

Education Before Market Participation

Before allocating personal funds, Mikhail completed the educational program and observed trading sessions conducted through the Profit Princess community.

His initial trading capital was USD 1,000, which he had accumulated before joining the program. According to the case study, Mikhail established several rules before beginning to trade. These included limiting the amount of capital used in individual positions, defining potential losses in advance, recording trading results, and stopping activity after reaching a predetermined daily loss limit.

The case study states that Mikhail experienced both profitable and unprofitable trades during the initial period. Rather than increasing position sizes after losses, he reviewed his decisions and continued studying the educational materials.

Mikhail also participated in community trading sessions where market situations and completed trades were analyzed. The purpose of these sessions was to help participants understand the reasoning behind trading decisions rather than encourage the automatic replication of individual positions.

According to Mikhail, maintaining discipline was particularly difficult because of the financial pressure affecting his family.

“When a family is dealing with debt, there is a strong temptation to make decisions quickly and take additional risks. The main principle emphasized during the training was to protect capital before focusing on potential profit,” Mikhail said.

Application of Predefined Risk Limits

During the four-week period described in the case study, Mikhail continued working at his regular job and traded during his available time.

Before each trading session, he established a maximum acceptable risk and a loss level at which he would stop trading. He also maintained records of his entries, exits, results, and reasons for making each decision.

The case study reports that this process helped Mikhail reduce impulsive decisions and identify recurring mistakes. It also allowed him to evaluate his activity based on adherence to a system rather than the result of a single trade.

Profit Princess emphasizes that risk management cannot eliminate the possibility of financial loss. Trading performance may be affected by market volatility, execution conditions, participant experience, emotional decisions, and other factors.

Reported Result After Four Weeks

According to account information provided for the case study, Mikhail’s trading balance increased from USD 1,000 to USD 5,500 over four weeks. The reported difference of USD 4,500 represented trading profit before considering any personal tax obligations that may apply.

Mikhail subsequently withdrew USD 3,500 and transferred the funds to his parents. The remaining trading balance was USD 2,000, consisting of his original capital and USD 1,000 in reported profit.

According to the participant, the withdrawn funds allowed the family to reduce its overdue balance and continue discussions regarding a revised repayment schedule. The payment did not eliminate all of the family’s financial obligations, but it provided additional time to address the remaining balance.

“The result was important because it gave the family an opportunity to stabilize the situation. It did not remove the need for continued work, careful budgeting, and further payments,” Mikhail said.

Focus on Process Rather Than Individual Returns

Profit Princess states that the case study is being published to demonstrate the importance of preparation, predefined limits, and emotional control. The company does not present Mikhail’s reported performance as typical or reproducible.

Lisa noted that individual financial results should not be separated from the time spent studying, reviewing mistakes, documenting decisions, and avoiding trades that did not meet established criteria.

“The final account balance is only one part of the case study. The more relevant element is the participant’s ability to follow predefined rules despite significant emotional pressure. Trading education should focus on responsible decision-making and risk awareness, not on promises of rapid income,” Lisa said.

Mikhail continues to work at his regular job and participate in financial market education. According to the case study, he does not currently plan to increase his trading volume substantially and remains focused on maintaining defined risk limits.

He also does not describe himself as a professional trader. His stated priorities are continuing his education, supporting his family, and avoiding decisions based on urgency or emotion.

Risk Disclosure

Trading in financial markets involves a substantial risk of loss and may not be suitable for every person. Participants may lose some or all of the capital allocated to trading.

The performance described in this case study represents the reported experience of one participant during a specific period. It should not be interpreted as a guarantee, forecast, investment recommendation, financial advice, or indication of future results.

Market conditions and individual outcomes vary. Anyone considering participation in financial markets should independently assess the risks, review applicable legal and tax requirements, and seek advice from a qualified financial professional where appropriate.

Media Contact

Organization: Profit Princess

Contact Person: Victoria Hayes

Website: https://t.me/+DwU5IXGj6ONmZTEy

Email: Send Email

Country:Belarus

Release id:47985

The post Profit Princess Publishes Trading Education Case Study Focused on Risk Management appeared first on King Newswire. This content is provided by a third-party source.. King Newswire makes no warranties or representations in connection with it. King Newswire is a press release distribution agency and does not endorse or verify the claims made in this release. If you have any complaints or copyright concerns related to this article, please contact the company listed in the ‘Media Contact’ section

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Quatre Bornes, Mauritius, August 08, 2026, ZEX PR WIRE — CapitalXtend has announced the launch of its refreshed identity and redesigned website, marking an important milestone in the company’s continued evolution. The update reflects CapitalXtend’s commitment to creating a more modern, accessible, and client-focused trading experience while strengthening the foundation for its next phase of growth.

This represents more than a visual update. It reflects CapitalXtend’s ongoing investment in improving how traders engage with the company across every touchpoint. Alongside the new identity, the redesigned website introduces a cleaner interface, improved navigation, and a more intuitive structure, making it easier for both new and existing clients to explore the company’s products, platforms, and trading services.

The enhanced digital experience enables traders to access account information, compare trading solutions, explore platform features, and navigate market opportunities with greater ease. Every improvement has been designed to simplify the user journey while maintaining the professional standards, reliability, and performance for which CapitalXtend is known.

This milestone also reinforces CapitalXtend’s broader commitment to innovation and continuous improvement. By refining its digital experience and strengthening the way traders interact with the brand, CapitalXtend continues to invest in making its services more accessible, intuitive, and user-focused. As part of its offering, traders continue to benefit from solutions such as CFD Shares, Holders Account, Return on Equity, and Unlimited Leverage.

Existing clients will experience a seamless transition, with no changes to account credentials, funds, or account types. The updated platform allows traders to continue operating without interruption while benefiting from a more refined digital environment.

Speaking on the milestone, Dr. Farrukh Adeeb, Group CEO & Chairman of XGroup, said:

“This is an important milestone for CapitalXtend. Our refreshed identity reflects how the company has evolved and where we are heading next. Beyond a new look, this launch represents our continued investment in delivering a better experience for our clients, making it simpler to access our services, navigate our platform, and trade with confidence as we continue to grow.”

The website is now live, representing another step in the company’s journey to deliver a trusted, innovative, and client-centric trading experience for its global community.

About CapitalXtend

CapitalXtend is a global multi-asset broker committed to delivering a secure, transparent, and technology-driven trading experience. Offering access to a wide range of financial markets through advanced trading platforms, the company continues to focus on innovation, client-centric service, and empowering traders with reliable trading solutions.

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Press Release

Grepix Infotech Highlights White Label Apps as a Smart Business Model for On-Demand Entrepreneurs

Grepix Infotech shares industry insights on how enterprise-grade white label technology is helping entrepreneurs launch faster, reduce technology costs, and compete in the growing on-demand economy.

Noida, Uttar Pradesh, India, 8th Aug 2026 — Grepix Infotech Pvt Ltd, a globally recognised on demand technology company powering app businesses across 30+ countries, today published its industry perspective on the question every technology entrepreneur eventually faces: do you build your own platform from scratch, or do you launch faster and smarter using a proven white label solution?

For entrepreneurs targeting the on demand economy in 2026 — one of the fastest-growing and most competitive commercial landscapes in the world — the answer has never been clearer.

A $600 Billion Market With No Room for Slow Movers

The global on-demand economy is now valued at over USD 600 billion and growing at a compound annual growth rate of over 18 percent. From ride-hailing giants like Uber, Bolt, and Didi to food delivery leaders like DoorDash, Glovo, and Jumia Food, the playbook has been written. Consumers in every market — from São Paulo to Kuala Lumpur, Karachi to Cairo, and Manila to Mexico City — have already formed on-demand habits. They expect instant service, real-time tracking, and seamless digital payments as a baseline — not a luxury.

The opportunity for regional entrepreneurs is enormous. The platforms dominating global headlines are not winning in every city, every town, or every emerging market corridor. There are thousands of underserved markets across Asia, Africa, Latin America, Eastern Europe, and the Middle East where a fast-moving, locally operated on-demand business can capture significant market share — if it gets there fast enough.

That is exactly where white label technology changes the game entirely.

Why Most On-Demand Startups Never Make It to Launch

Across hundreds of client engagements spanning markets from Dhaka to Dubai, Bogotá to Bangkok, and Accra to Auckland, Grepix has observed a consistent and sobering pattern: the most common reason on-demand startups fail is not a flawed business model or insufficient funding. It is the time, cost, and complexity of building the technology itself.

Building a competitive ride-hailing platform — with a passenger app, driver app, admin panel, real-time GPS dispatch, dynamic surge pricing, and multi-gateway payment integration — requires a minimum development timeline of 10 to 14 months and a budget typically ranging between USD 40,000 and USD 100,000, depending on team quality and feature scope. That figure excludes ongoing maintenance, server infrastructure, security updates, and the continuous feature development required to stay competitive in a rapidly evolving market.

By the time a custom-built app launches, a competitor running on a proven white label platform has already acquired drivers, signed up restaurants, onboarded service providers, and locked in early customer loyalty.

“We have seen brilliant entrepreneurs with the right market insight, the right capital, and the right team — completely derailed by a development cycle that consumed 18 months and twice their planned budget. By launch day, someone else already owned the market,” said a spokesperson for Grepix Infotech. “The technology timeline does not just slow a business down. It can kill it entirely.”

What Modern White Label Actually Delivers

The white label model of 2026 bears no resemblance to the generic, off-the-shelf software of a decade ago. Today’s enterprise-grade white label platforms like those built by Grepix offer full source code ownership, complete brand identity customisation, region-specific feature configuration, dedicated technical onboarding, and continuous product updates informed by real-world deployments across diverse global markets.

Entrepreneurs who choose white label do not receive a template. They receive a battle-tested, commercially proven technology foundation that has already processed millions of transactions, resolved thousands of edge cases, and been refined across deployments in markets as diverse as Saudi Arabia, Brazil, Vietnam, Ghana, Turkey, and Colombia.

A white label deployment through Grepix can be live in under two weeks at a fraction of the cost of custom development with zero compromise on quality, scalability, or brand identity.

Speed to Market is the Real Competitive Moat

In the on-demand economy, first-mover advantage is not a cliché. It is a commercial reality.

The platform that signs up drivers first, the aggregator that onboards restaurants before anyone else, and the logistics operator that locks in enterprise clients early — these businesses build supply and demand flywheels that are expensive and time-consuming for any competitor to replicate. Just as Bolt disrupted Uber across multiple markets by moving fast and operating with local agility, and just as Grab built a dominant super app position across Southeast Asia by prioritising speed of market penetration over perfection of technology, regional entrepreneurs can carve out dominant positions in their own cities and countries — if they launch before the window closes.

White label eliminates the development delay entirely. Rather than spending a year building, entrepreneurs can redirect every dollar and every hour into driver acquisition, restaurant partnerships, hyperlocal marketing, and customer experience — the activities that actually determine whether an on-demand business survives and scales.

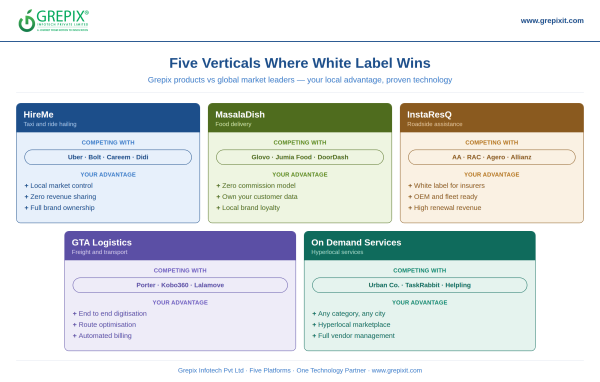

Five Verticals Where White Label Delivers the Strongest ROI

Ride Hailing and Taxi — Where Uber, Bolt, and Careem dominate at a global scale, hundreds of city-level and country-level markets across Indonesia, Morocco, Kazakhstan, Peru, and Senegal remain open to locally operated alternatives. Grepix’s HireMe taxi app platform gives entrepreneurs a fully branded, Uber-class ride-hailing business with intelligent dispatch, surge pricing, and real-time GPS tracking — deployable in days, not months.

Food Delivery — As Glovo, Jumia Food, Talabat, and DoorDash expand across markets from Istanbul to Lagos and from Riyadh to Ho Chi Minh City, the demand for locally owned and zero commission alternatives is accelerating rapidly. Grepix’s MasalaDish food delivery platform lets entrepreneurs launch a fully independent food delivery business — retaining complete control of margins, customer data, and vendor relationships in a way the large aggregators will never offer.

Roadside Assistance — A high renewal, high retention vertical with strong demand from insurance companies, automobile manufacturers, and fleet operators across markets including the UAE, South Africa, Malaysia, Argentina, and Egypt. Grepix’s InstaResQ Roadside Assistance platform connects stranded drivers to the nearest verified service provider in minutes — white labeled and fully brandable for any insurer, OEM, or fleet operator entering this space.

Logistics and Freight — As platforms like Porter, Kobo360, Lalamove, and Trukker have demonstrated across India, Nigeria, Hong Kong, and the UAE, digitising freight logistics is a multi-billion-dollar opportunity in every emerging and developing market on the planet. Grepix’s GTA Logistics platform gives logistics entrepreneurs a complete digital freight operation — booking, real-time fleet tracking, route optimisation, proof of delivery, and automated billing — without a single line of custom code, ready to compete from day one.

Home and Hyperlocal Services — In markets where Urban Company, TaskRabbit, Helpling, and Handyman have proven the hyperlocal services model across India, the United States, Germany, and the United Kingdom, the opportunity for locally operated equivalents across Thailand, Nigeria, Chile, Jordan, and the Philippines remains wide open and largely uncontested. Grepix’s On Demand Services platform enables entrepreneurs to launch a fully configured hyperlocal marketplace across any home service category — cleaning, beauty, appliance repair, healthcare — in virtually any city, in virtually any market, within days.

White Label Is Not a Shortcut — It Is a Growth Strategy

The most successful franchise and platform businesses in the world — from global fast food networks to logistics giants — do not build proprietary technology stacks from the ground up. They adopt proven operational systems, focus investment on local execution, and compete on customer relationships and market knowledge.

White label on-demand technology follows exactly the same principle. The entrepreneurs winning in the on-demand space in 2026 are not the best developers. They are the best operators — and white label gives them the technology infrastructure to operate at full commercial scale from week one, in any city, in any country, with any brand name they choose.

For any entrepreneur evaluating entry into the on-demand economy, the question is no longer whether white label is credible or capable enough. The question is whether they can afford the capital burn, the time delay, and the competitive risk of not using it.

About Grepix Infotech Pvt Ltd

Grepix Infotech Pvt Ltd is a New Delhi-based technology company and the developer behind HireMe, MasalaDish, InstaResQ, GTA Logistics, and the Grepix On Demand Services Platform. With 500+ clients across 30+ countries and over a decade of product development experience, Grepix is the white label technology partner of choice for entrepreneurs and enterprises building on-demand businesses across Africa, the Middle East, South Asia, Southeast Asia, and Latin America.

Media Contact

Organization: Grepix Infotech Pvt. Ltd.

Contact Person: Vinay Jain

Website: https://www.grepixit.com

Email: Send Email

Contact Number: +918860213347

Address:Logix Technova A 328, Noida-Greater Noida Expy, Block B, Sector 132, Noida, India – 201304

City: Noida

State: Uttar Pradesh

Country:India

Release id:47948

The post Grepix Infotech Highlights White Label Apps as a Smart Business Model for On-Demand Entrepreneurs appeared first on King Newswire. This content is provided by a third-party source.. King Newswire makes no warranties or representations in connection with it. King Newswire is a press release distribution agency and does not endorse or verify the claims made in this release. If you have any complaints or copyright concerns related to this article, please contact the company listed in the ‘Media Contact’ section

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Profit Princess Publishes Trading Education Case Study Focused on Risk Management

CapitalXtend Launches New Brand Identity and Enhanced Digital Experience

Grepix Infotech Highlights White Label Apps as a Smart Business Model for On-Demand Entrepreneurs

Benzinga Money Article Discusses How to Become Part of the 12% of Retirees Who Have Achieved the Recommended $550,000 Minimum Retirement Savings Threshold

Apu Apustaja Conquers New York with Lively Street Ads, Including Times Square Billboard

Bay Smokes Maintains Quality Amid Legislative Changes in the Hemp Industry

-

Press Release3 days ago

STARTRADER in Discussions with Trustpilot to Consolidate Review Profiles

-

Press Release3 days ago

Fire Safety Innovation in the Spotlight as Industry Expert Paul Trew Speaks Out on Evolving Fire Risk

-

Press Release5 days ago

Global Hit Anime Jaadugar: A Witch in Mongolia Unveils 3rd Main PV and Visual, Kujira as 1st Empress

-

Press Release7 days ago

Rasmala Global Sukuk Fund Named Winner of Two 2026 LSEG Lipper Fund Awards for Best Fund over 10 Years

-

Press Release3 days ago

Social Security Adjustments Have Failed to Keep Pace with Inflation—How Retirees Can Supplement Their Income Through Bitcoin Mining in 2026

-

Press Release4 days ago

From a Free Book to a Business in the Making: Entrepreneur Vanessa Murphy Launches Trading My Way Barter Journey Across the U.S.

-

Press Release2 days ago

Movement, El Vecino and RISE Partner to Launch First Digital Dollar Wallet for Mexican Remittances

-

Press Release2 days ago

AI Expert Amol Walvekar Builds First-Ever RAG-Powered, Custom AI for Finance Processes