Press Release

“Algorithm + Credit” Rebuild the Value Foundation of DeFi

DeFi still has higher attention, with rapid technological innovation and continuous expansion of application scope, The goal of DeFi is undoubtedly to build a more effective, free, and transparent financial ecology. However, finance always develops with money and brings value exchange. Therefore, whether it is a decentralized scenario or a mass application toward reality in the future, stable cryptocurrency is crucial for users, so as to realize the dream of making virtual ideas become reality.

For this reason, in the field of cryptocurrency, many teams have been exploring stable currency. According to CryptoQuant data, stabilecoin holdings on global crypto exchanges hit a high record of $9.8 billion as of March 28, 2021. At the same time, the total stable currency market capitalization once topped $80 billion, according to CoinGecko, the current daily trading volume of all stable currencies is about $118.340 billion. Also, CoinMarketCap shows there are 16 mainstream stable currencies now.

The stable currency is illusory?

In general, both USDT and DAI are still on their way and haven’t really achieved the goal of “stable currency”. Tether’s White Paper said: “Tether is a decentralized cryptocurrency, but we are not a perfectly decentralized company. We store all of our assets as a centralized pledge.” Therefore, USDT is just borrowing the name of the cryptocurrency, but it is not really decentralized.

DAI, developed by MakerDao, is the largest decentralized stable currency on Ethereum. It is issued with the guarantee of the full amount of assets on the blockchain. It is only generated in the application scenario based on the mortgage, and the market value of the mortgage assets is the ceiling of it. Therefore, these stable currencies are illusory in a sense.

Will algorithmic stable currencies finally fail?

Now let’s take a look at the development process of algorithmic stable currencies, known as the holy grail of cryptocurrency. From stable currency1.0 represented by AMPL, stable currency2.0 represented by Basis Cash to stable currency 3.0: Frax Finance, all of them have gone through a period of growth. However, the stable currency reality is that we live under the sense of “ever-changing”, and stable value is still in the ideal.

AMPL algorithmic stable currency is used to increase or decrease the supply of AMPL in order to keep the price of AMPL around $ 1. Ampleforth uses Rebase operation to change the AMPL held by all users as a whole. The Rebase price is based on the average price of the past 24 hours. When this price is above $1.05, the AMPL balance in all users’ wallets increases simultaneously. At prices below $0.95, all users’ AMPL balances decrease simultaneously. During this process, the percentage of AMPL held by users in the supply does not change. It looks like everything is fine on its own, but when the price of cryptos falls to the point where deflation is needed, both the quantity and price of coins held by users are falling, so users face a double whammy.

So it’s easy to create a death spiral. Similarly, when crypto price rises, it is easy to create an upward death spiral. Thus it can be seen that this price model only has two possibilities: the price continues to fall, get into the infinite death circle and leave the market, and the price rises steadily to around 1USDT; Prices rising, the AMPL has been printing (dividend), AMPL reserve disappeared, crypto began to value return, people in loss cannot gain AMPL, prices will fall back near 1 USDT (need funds continue getting into the market), so it is difficult to see AMPL achieve speculation, meanwhile achieve stability, And stability is a necessary condition for a stable currency.

Basis Cash, as represented by 2.0, includes three tokens, Basis Cash (BAC), Basis Share (BAS), and Basis Bond (BAB), among which BAB is non-transferable. The BAC is the stable currency, anchored to $1; BAS is an equity token, and newly-minted BAC tokens can be allocated. BAB is a bond. There is nothing wrong with Basis Cash based on the algorithm itself, but without a good application scenario, relying on the debt market itself is dangerous. There is actually a problem with debt financing in traditional markets, where those “too big to fail” entities can take on the risk of impunity through socialized bailout costs. It is entirely possible that Basis Cash could go into a debt spiral, in which case there would be no willing contributors, the debt would accumulate and the protocol would collapse.

Finance FX is the first partial algorithmic stable currency project, adding the concept of using “partially stable” as a collateral asset to the existing algorithmic stable currency. There are two types of tokens in Frax, the stabilization token Frax, and the governance token FXS. Frax costs USDC and FXS, but only USDC during creation. The initial mortgage rate is 100%, that is, all USDC mortgage is used to cast FRAX. After that, the mortgage rate will be adjusted every hour. If the price of FRAX is more than $1, the mortgage rate will be reduced and FXS ‘share in it will be increased. Raise the mortgage rate if the Frax falls below $1. The mortgage rate is adjusted every hour by 0.25% each time. But its high mortgage ratio leads to the lack of user appeal, its currency numbers and market supply have been stagnant.

Although the above three generations of stable currencies seem to be making breakthroughs and innovations, they do not give a satisfactory answer on how to solve the credit problem. However, algorithm stable currency that cannot solve the credit problem is useless. Bitcoin came into being to solve the problem of credit, but the stable currency, as an important extension of its development, has not inherited the legacy of credit, and is still stuck in the algorithm.

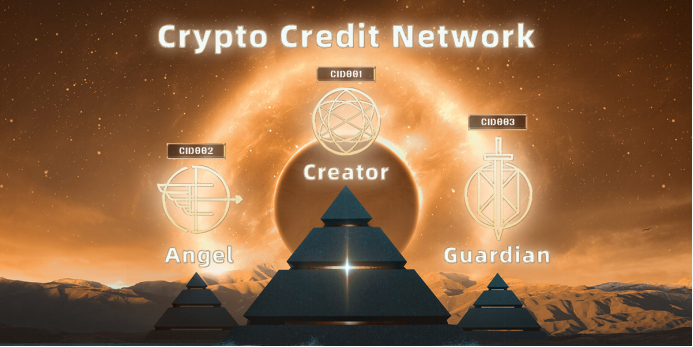

Crypto Credit Network (CCN)

In the financial field, credit is the foundation and the lifeblood. This is true of both traditional and modern financial systems. In the traditional financial system, credit mainly relies on the guarantee of laws and institutions. Apart from the high operation cost, the “credit crisis” gradually exposed by financial intermediaries is the fundamental reason why people urgently embrace the blockchain technology. Algorithm stable currency is going to help cryptos solve the credit problems, guaranteeing machine credit by algorithm, which does not rely on third-party subjective will and makes transaction transparent, efficient, reliable, and stable, let people who do not have to establish credit relationship between each other to achieve cooperation and free trading, reduce the cost of credit.

However, the world of blockchain cryptocurrency is a chaotic existence without a role name. To change from chaos to brightness, each individual needs to have his or her own identity, so that we can obtain the faith like phoenix nirvana. The CCN gives each individual a unique CID (Crypto Identification), which is the most basic rule in the Crypto world. To build a new crypto world of order, autonomy, and equality.

The construction of CCN not only takes blockchain technology as support, but also has a reasonable economic incentive mechanism. Reasonable use of incentive mechanism is an effective means to stimulate all parties to participate in the construction of CCN.

A sound incentive mechanism, reasonable mechanism design from the perspective of leading efficiency and fair governance, can make the value generated by credit information flow effectively to the value provider in the blockchain world, punish the evil behavior, and resolve the conflict between individual interests and collective interests. It makes the individual’s behavior of pursuing individual interests unified with the goal of maximizing collective value.

Therefore, CCN can further clarify the economic interests of each participant and the overall interests of the network, so as to fully mobilize the enthusiasm of each participant and guarantee great development of CCN from the source.

The CCN consists of three different identities: Creator, Guardian, and Angel, all of them have established screening mechanisms. Only firm believers can obtain the CCN identity. Early believers are required to contribute to maintaining the stability of early CCN by burning GAC tokens. Therefore, they are not only holders of GaeaCoin, but also determined preachers and builders. When GaeaCoin issues additional shares, it will also receive a corresponding percentage of GAC tokens as a reward.

The establishment of this system aims to provide every GaeaCoin participant with the opportunity to contribute to the community construction, and to create a healthy crypto community culture of dedication and autonomy through consensus, symbiosis, co-construction, and sharing.

In CCN, although the identity is different, the residents on the chain of CCN build the initial transaction link according to their CID address, and constantly expand CCN on the chain. Open CID needs to be recommended by the network resident, once the link is formed, it cannot be changed forever. Each of the three different identities requires a different number of GAC tokens to burn, which can be viewed on the GaeaCoin network. GaeaCoin network residents have different rights according to their status.

The integration with the DEX: OxySwap has pioneered a full range of applications

There is a natural interdependence between exchange and stable currency. The exchange has always been an important part of crypto digital asset market, and it is also the first application place of stable currency. Like Binance with BUSD and Huobi with HUSD, OKEx also launched USDK on June 3, 2019. Traditional CEXs are fiat currencies, where fiat currencies are exchanged for cryptos. If you want to buy crypto digital assets, you need to top up fiat currency, which undoubtedly increases the economic and time costs of investors in the process of exchange. The emergence of a stable currency can not only solve the above problems but also effectively avoid legal risks in the process of the transaction.

As it should be, the integration of GaeaCoin ecology and OxySwap not only lay a solid foundation for stable currency: GAC token application, but also creates opportunities for it to open up more and wider application scenarios.

OxySwap is a decentralized exchange running on the BSC with a collection of DEX liquidity mining, which offers functions of exchange, liquidity, market making, and so on. The strength of OxySwap guarantees the usages of the stable currency: GAC.

GAC will lead a brighter way

GaeaCoin algorithm stable currency: GAC dares to face the challenge, according to the industry news, GAC praises is not only relatively stable from the concept, but also to really put into application. In addition to GAC (GaeaCoin), GaeaCoin ecology also includes GAB (GaeaCoin Bond) and GASH (GaeaCoin Share), which serve to maintain the stability of GAC. GaeaCoin Ecology also integrates GaeaCoin protocol, algorithm, robustness, price response, encryption, and other technologies, superposed with the DeFi ecology of Crypto Credit Network (CCN), OxySwap (DEX), and so on, providing a realistic solution for GAC, and leads it to move towards the real “stability”.

The integration of CCN and OxySwap points out the direction for the application of algorithmic stable currency. In fact, we can already feel the power of the GaeaCoin algorithm stable currency, and once it is used at a large scale, the ideal stable currency is expected to arrive ahead of time. DeFi will also build on this basis, using currency, lending, spot trading, and other components to build continuously upgraded Lego of DeFi.

GaeaCoin’s move directly challenges the world’s centralized stable currency giants such as USDT and USDC, but compared to the previous challenges of AMPL, BAC, and FRAX, this well-prepared challenge looks more anticipated!

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Naples, FL, USA, August 11th, 2026, FinanceWire

Drones have become a growing security problem, and the market to stop them is expanding just as quickly. MarketsandMarkets estimates the global counter-unmanned aircraft systems market will grow from $6.64 billion in 2025 to $20.31 billion by 2030, representing a 25.1 percent compound annual growth rate. Within that forecast, AI-powered counter-UAS is the fastest-growing technology layer, projected to expand from $0.9 billion in 2025 to $6.2 billion by 2030. As governments and critical infrastructure operators look for ways to detect, track, and defeat increasingly sophisticated drone threats, defense companies are racing to build the next generation of counter-UAS technology. Several public companies are already staking positions in counter-UAS, approaching the opportunity from different angles.

Change Agents Corp. (Nasdaq: CHGA) has joined the Institute for Defense and Government Advancement, or IDGA, and will take part in the organization’s Counter UAS Summit. Now in its eighth year, the summit runs August 25 to 26 at the MGM National Harbor in Maryland under the chairmanship of retired General Glen VanHerck, former commander of North American Aerospace Defense Command and U.S. Northern Command. IDGA expects more than 500 senior decision-makers, acquisition leaders, and program managers from the Army, Navy, Air Force, Marines, Customs and Border Protection, and law enforcement, placing Change Agents in direct contact with the buyers and technology developers shaping counter-drone procurement.

The summit role builds on the company’s August 4 launch of Autonomous Air Defense LLC, a wholly owned subsidiary formed to identify, evaluate, acquire, and develop autonomous air defense and counter-UAS technologies. That announcement also brought retired Major General Malcolm Frost onto the advisory boards of both Change Agents and the new subsidiary. Frost served 31 years in the U.S. Army, retiring as a two-star general after commanding the 2nd Stryker Brigade Combat Team of the 25th Infantry Division and serving as Deputy Commanding General of the 82nd Airborne Division. He is a West Point and Army War College graduate who deployed to Bosnia, Iraq, and Afghanistan, and he advises public and private companies across the defense and technology sectors.

Change Agents built its business in agentic AI software, pairing an AI search optimization platform called Beacon with an autonomous content creation platform called Catch-Up, both sold on a subscription model. Management frames the counter-drone move as an outgrowth of that work rather than a break from it. Director Michael Mathews called the formation of Autonomous Air Defense LLC “a natural extension of the company’s broader artificial intelligence strategy” and tied the IDGA engagement to positioning the company to “capitalize on the significant long-term opportunities within the global counter-UAS market. ” Frost, in joining, pointed to the convergence of artificial intelligence, autonomous systems, and next-generation counter-drone technology as one of the most important developments in modern defense.

That convergence is the opening Change Agents intends to pursue, and the sequence so far has been deliberate. In roughly a week the company has stood up a dedicated subsidiary, added a decorated defense advisor, and secured a place at the sector’s principal U.S. gathering. The company has said Autonomous Air Defense is evaluating multiple acquisition and partnership opportunities involving AI-enabled counter-drone technologies serving defense, homeland security, and critical infrastructure customers, and that it expects to provide further updates as developments occur.

Change Agents is entering a field already populated by well-funded public companies attacking the drone problem from different angles.

Ondas Inc. (Nasdaq: ONDS) is the closest analog to what Change Agents describes. Its Iron Drone Raider is an autonomous net-based interceptor built to neutralize hostile drones without jamming, paired with its Sentrycs platform for cyber and radio-frequency detection and identification, together mirroring the detect, identify, track, and intercept sequence Change Agents has said it wants to reach. Ondas posted first-quarter 2026 revenue of $50.1 million against a pro forma backlog of $457 million and in July raised its full-year 2026 revenue target to at least $525 million. In February its Airobotics subsidiary secured a multi-million-dollar order from a European customer in a NATO country following an Iron Drone Raider deployment at a major international airport, one of the few operational uses of an interceptor drone in a live civil-aviation setting.

AeroVironment (Nasdaq: AVAV) approaches the market as an established contractor. Its acquisition of BlueHalo, valued at roughly $4.1 billion and completed in May 2025, added directed energy, electronic warfare, and counter-UAS capabilities to a portfolio already known for the Switchblade family of loitering munitions. BlueHalo had delivered its 1,000th Titan radio-frequency counter-UAS system before the deal closed and was the first to operationally field a laser weapon system with LOCUST. The combination turned a former drone specialist into a diversified defense technology platform spanning radio-frequency, directed energy, and kinetic defeat, and it marks the scaled version of the category Change Agents is entering.

Kratos Defense & Security Solutions (Nasdaq: KTOS) anchors the autonomous systems end of the field. Best known for the jet-powered XQ-58A Valkyrie, Kratos reported second-quarter 2026 revenue of $458.8 million, up 30.5 percent year over year and 19.1 percent organically, and raised full-year 2026 guidance to a range of $1.75 billion to $1.81 billion. Total backlog stood at $2.084 billion against a bid pipeline of $15.0 billion, a measure of how much defense money is now moving through unmanned and autonomous programs, and of the budgets, Change Agents is positioning to reach.

Ondas, AeroVironment, and Kratos map the opportunity from interceptor specialist to diversified prime, and they mark out the market Change Agents Corp. (Nasdaq: CHGA) has chosen to enter. What CHGA has established is a subsidiary, an advisor with two-star command experience, and access to the procurement community setting counter-drone requirements. What remains prospective is the technology itself, and the company has said it expects to report further developments as it works through the acquisition and partnership opportunities in front of it.

Disclaimers: RazorPitch Inc. “RazorPitch” is not operated by a licensed broker, a dealer, or a registered investment adviser. This content is for informational purposes only and is not intended to be investment advice. The Private Securities Litigation Reform Act of 1995 provides investors a safe harbor in regard to forward-looking statements. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, goals, assumptions, or future events or performances are not statements of historical fact and may be forward-looking statements. Forward-looking statements are based on expectations, estimates, and projections at the time the statements are made that involve a number of risks and uncertainties that could cause actual results or events to differ materially from those presently anticipated. Forward-looking statements in this action may be identified through the use of words such as projects, foresee, expects, will, anticipates, estimates, believes, understands, or that by statements indicating certain actions & quote; may, could, or might occur. Understand there is no guarantee past performance will be indicative of future results. Investing in micro-cap and growth securities is highly speculative and carries an extremely high degree of risk. It is possible that an investor’s investment may be lost or impaired due to the speculative nature of the companies profiled. RazorPitch has been retained and compensated by Change Agents Corp to assist in the production and distribution of content related to CHGA. RazorPitch is responsible for the production and distribution of this content. It should be expressly understood that under no circumstances does any information published herein represent a recommendation to buy or sell a security. This content is for informational purposes only; you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by RazorPitch or any third-party service provider to buy or sell any securities or other financial instruments. All content in this article is information of a general nature and does not address the circumstances of any particular individual or entity. Nothing in this article constitutes professional and/or financial advice, nor does any information in the article constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. RazorPitch is not a fiduciary by virtue of any persons use of or access to this content.

Contact

Mark McKelvie

RazorPitch

mark@razorpitch.com

585-301-7700

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

San Francisco, California, USA, August 11th, 2026, FinanceWire

The ranking validates HoneyBook’s growing reputation as an innovator accelerating the digital transformation of independent businesses globally

HoneyBook, the leading AI-native client relationship platform for small business owners, has been recognized as one of the world’s most significant financial technology firms in CNBC’s 2026 list of the World’s Top Fintech Companies. Its inclusion in the prestigious global list within the Enterprise Fintech category underscores the impact that HoneyBook’s software has had in helping individual business owners to cultivate strong customer relationships.

Produced in partnership with Statista, CNBC’s list is a recognized annual ranking that serves to highlight the world’s most innovative and forward-thinking financial software firms. As part of its assessment process, CNBC evaluates thousands of eligible firms, ranging from startups to established enterprises, based on key performance indicators such as revenue and user growth, transaction volume, business impact and technological innovation. HoneyBook’s debut on this year’s list reflects growing recognition of its platform.

HoneyBook is noted for accelerating automation in the customer relationship management software niche, helping business and freelancers to better manage their day-to-day dealings with clients. Its platform frees users from spending hours on critical business tasks such as capturing and verifying inquiries, drafting proposals, obtaining signatures on contracts, sharing files with customers and processing transactions. With HoneyBook, business owners can manage their administrative and financial operations in a unified platform, making use of autonomous AI agents to perform work they once spent hours on. By linking client communications with financial operations, HoneyBook helps business professionals to work more efficiently and get paid promptly.

CNBC’s recognition of HoneyBook follows the rapid expansion of its client relationship platform into new verticals. Last month, HoneyBook launched a dedicated version of its CRM platform for professional photographers, featuring specialized tools for client bookings, creating schedules, managing their galleries and collaborating with clients on projects. With HoneyBook, photographers get more time to focus on their clients and their work instead of worrying about the administrative side of their business.

“I’m extremely proud that our endeavors to enhance and simplify client relationships have led to HoneyBook being recognized by CNBC as one of the world’s best fintech companies,” said Oz Alon, co-founder and Chief Executive Officer of HoneyBook. “By enabling business owners to nurture relationships with clients in the same place as they manage their finances, HoneyBook significantly reduces the complexity they face when using multiple fragmented tools. CNBC’s recognition validates our ability to empower independent entrepreneurs with innovative tools that streamline the day-to-day aspects of business management.”

About HoneyBook

HoneyBook is the leading AI-powered customer relationship management (CRM) platform for independent business owners, making it easy to sell and deliver their services online. Offering powerful tools for communication, contracts, invoicing, payments and more, the platform puts independent professionals in control of their process and client experience. HoneyBook is trusted by over 100,000 service-based businesses in the United States, Australia, Canada, and the United Kingdom that have booked more than $10 billion in business on the platform. The company has offices in San Francisco and Tel Aviv, with remote staff worldwide. Learn more at HoneyBook.com.

Contact

Dan Edelstein

InboundJunction

pr@inboundjunction.com

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Press Release

Organization Launches Executive Leadership Insights Series Featuring Brent Byng on Turning Strategy Into Measurable Results

Navarre, Florida, Aug 11, 2026, ZEX PR WIRE — Organizations across industries continue to face mounting pressure to deliver measurable outcomes while navigating economic uncertainty, technological disruption, and evolving workforce expectations. To address these challenges, an executive leadership insights series has been launched featuring senior operations executive and military leader Brent Byng, focusing on how organizations can successfully transform strategic vision into operational results.

The initiative, titled “From Strategy to Execution: Brent Byng on Turning Vision Into Measurable Results” will examine practical approaches to organizational performance, leadership accountability, operational planning, and enterprise execution. Drawing on more than 28 years of leadership experience spanning military operations, strategic planning, analytics, and organizational transformation, Byng will contribute insights designed to help leaders bridge the gap between ambitious goals and measurable outcomes.

The announcement comes at a time when organizations are increasingly seeking proven methods to improve execution, strengthen accountability, and align resources with strategic priorities.

Addressing a Common Organizational Challenge

Many organizations invest significant time developing strategic plans, yet struggle to translate those plans into sustained results. Leadership teams often establish ambitious goals but encounter obstacles when attempting to align people, processes, technology, and resources around those objectives.

The executive leadership insights series aims to address this challenge by exploring the practical side of execution. Rather than focusing exclusively on strategic vision, the initiative highlights the systems, structures, and leadership practices required to transform ideas into measurable performance.

Byng’s career offers a unique perspective on this topic. Throughout his leadership journey, he has consistently operated in environments where successful execution carried significant consequences. Whether overseeing large-scale operations, managing multimillion-dollar budgets, or coordinating international partnerships, measurable outcomes remained the standard by which success was evaluated.

The initiative seeks to provide leaders with practical examples and lessons that can be applied across public and private sector organizations.

The Importance of Alignment

One of the central themes of the series focuses on organizational alignment.

According to Byng, execution becomes significantly more effective when teams understand not only what they are expected to accomplish but also why those objectives matter. Alignment requires more than communication. It requires connecting strategic priorities to everyday actions across every level of an organization.

Throughout his career, Byng has led organizations involving hundreds of personnel, multiple departments, and geographically dispersed operations. In those environments, maintaining alignment required clear goals, consistent communication, and performance systems that allowed leaders to monitor progress and adjust when necessary.

The initiative will examine how organizations can improve visibility, create accountability, and ensure that strategic objectives remain connected to operational activities.

Building Systems That Support Results

The leadership series will also explore the role of systems in organizational performance.

Byng has long advocated for building repeatable processes that enable consistent execution. During his leadership assignments, he implemented performance dashboards, forecasting models, training modernization programs, and operational reporting systems designed to improve decision-making and increase efficiency.

Rather than relying on individual effort alone, he focused on creating systems that allowed organizations to perform consistently over time.

This philosophy proved particularly valuable while leading large-scale training operations that supported thousands of personnel annually. Small inefficiencies often became significant obstacles when multiplied across large organizations. By improving workflows, introducing automation, and leveraging performance metrics, teams were able to improve outcomes while maintaining quality standards.

The initiative will highlight how organizations can use similar principles to support growth, improve productivity, and strengthen operational performance.

Data and Accountability Drive Better Decisions

Another key area of focus involves the growing role of data in leadership.

Modern organizations generate more information than ever before. Yet many leaders continue to struggle with transforming that information into actionable insights. The executive leadership series emphasizes the importance of creating reporting structures that support informed decision-making rather than overwhelming leaders with unnecessary complexity.

Byng’s experience includes managing operating budgets approaching $100 million while overseeing large-scale enterprise operations. In those roles, performance metrics, forecasting models, and operational analytics became essential tools for evaluating progress and allocating resources effectively.

The initiative will explore how organizations can build performance visibility into daily operations, allowing leaders to identify trends, address emerging issues, and make decisions with greater confidence.

Byng believes accountability becomes more effective when supported by clear information. When teams understand expectations and can measure progress against established goals, organizations are better positioned to achieve consistent results.

Leadership Beyond the Planning Process

While strategy development remains important, execution ultimately depends on leadership.

The series will examine how leaders influence organizational outcomes through communication, decision-making, and team development. Byng’s experience spans operational leadership, international diplomacy, strategic planning, and workforce development, providing a broad perspective on what drives organizational success.

As Special Assistant to the Chairman of the Joint Chiefs of Staff, Byng worked alongside senior defense officials, White House staff, and international partners to support strategic initiatives and strengthen cooperation among allied organizations. That experience reinforced the importance of translating complex objectives into actions that stakeholders could understand and execute.

The same principle applies in business environments. Leaders who communicate clearly and establish accountability structures are often better equipped to guide organizations through uncertainty and change.

Investing in People as a Strategic Priority

The initiative also recognizes that organizational success depends heavily on talent development.

Throughout his career, Byng has emphasized leadership development, mentoring, and succession planning as critical components of long-term performance. He believes organizations achieve stronger outcomes when employees understand their roles, develop new skills, and feel connected to larger organizational objectives.

The series will explore practical approaches to developing future leaders while creating cultures that encourage accountability, innovation, and continuous improvement.

As workforce expectations evolve and competition for talent increases, organizations continue searching for effective ways to attract, retain, and develop high-performing employees. Byng’s experience offers insight into how leadership development can support both individual growth and organizational performance.

Preparing Organizations for Future Challenges

The business environment continues to evolve rapidly. Advances in technology, changing customer expectations, workforce shifts, and economic uncertainty require organizations to remain adaptable while maintaining focus on long-term objectives.

The executive leadership insights series will examine how leaders can prepare their organizations for future challenges without losing sight of execution.

Byng believes organizations succeed when leaders balance vision with disciplined follow-through. Strategic planning provides direction, but measurable results emerge through consistent execution, accountability, and continuous improvement.

The initiative encourages leaders to view execution not as a final step in the strategic process, but as an ongoing responsibility that requires attention, adaptability, and commitment.

About Brent Byng

Brent Byng is a seasoned operations executive, senior military leader, and decorated U.S. Air Force officer with more than 28 years of leadership experience. Throughout his career, he has led organizations of more than 300 personnel, managed portfolios valued at nearly $100 million, and directed large-scale operational and training initiatives. His experience includes command leadership, enterprise operations, international partnerships, workforce development, and strategic planning. Byng holds advanced degrees in Operations Management, Military Operational Arts and Science, and Strategic Leadership, and he is currently pursuing a Doctor of Strategic Leadership.

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Counter-UAS Market Set to Triple by 2030 as Defense Companies Position for Growth

HoneyBook Included in CNBC’s 2026 List of the World’s Top Fintech Companies

Organization Launches Executive Leadership Insights Series Featuring Brent Byng on Turning Strategy Into Measurable Results

Benzinga Money Article Discusses How to Become Part of the 12% of Retirees Who Have Achieved the Recommended $550,000 Minimum Retirement Savings Threshold

Apu Apustaja Conquers New York with Lively Street Ads, Including Times Square Billboard

Bay Smokes Maintains Quality Amid Legislative Changes in the Hemp Industry

-

Press Release4 days ago

STARTRADER in Discussions with Trustpilot to Consolidate Review Profiles

-

Press Release10 hours ago

Demeter Tactical Investments (ME) Limited bolsters governance with two board appointments

-

Press Release4 days ago

Fire Safety Innovation in the Spotlight as Industry Expert Paul Trew Speaks Out on Evolving Fire Risk

-

Press Release4 days ago

Social Security Adjustments Have Failed to Keep Pace with Inflation—How Retirees Can Supplement Their Income Through Bitcoin Mining in 2026

-

Press Release6 days ago

Global Hit Anime Jaadugar: A Witch in Mongolia Unveils 3rd Main PV and Visual, Kujira as 1st Empress

-

Press Release5 days ago

From a Free Book to a Business in the Making: Entrepreneur Vanessa Murphy Launches Trading My Way Barter Journey Across the U.S.

-

Press Release6 days ago

Borderless.xyz Teams Up with Mastercard to Advance Trusted Cross-Border Stablecoin Payment Flows

-

Press Release4 days ago

Movement, El Vecino and RISE Partner to Launch First Digital Dollar Wallet for Mexican Remittances