Press Release

ACI quantitative robot-The power of reading the trends

In 1962, Everett-Rogers proposed the theory of innovative diffusion, designed to explain how, why, and how quickly new ideas and technologies were spread. The theory explains how a product or technology gains momentum and spreads across a specific population over time. The end result is that people apply a product, technology, or idea. One of the key implications is that the application of a new technology in the population does not occur simultaneously. Instead, certain people and groups are more likely to apply technology at different times, consistent with specific psychological and social characteristics. There are five established applicationcategories for new ideas or products. These categories are defined below.

A The Innovator. “Innovators are adventurous and willing to take the risks. They fundamentally wanted to be the first person to try something new. Their goal is to explore new technologies or innovation and to find opportunities to be drivers of change. 」

B Early App. “Once the benefits of a new innovation start to become obvious, early apps are eager to try. Early apps bought new technology to achieve revolutionary breakthroughs that gave them a huge competitive advantage in their industry. They like to gain more advantages than their peers, and they seem to have the time and money to invest. 」

C Early majority. “The early majority of the mainstream usually focused on innovation in solving specific problems. They look for complete products that are fully tested, adhere to industry standards, and are used by others they know in the industry. They are looking for gradual, proven ways to do what they are already doing. 」

D Later majority. “The late most are risk aversion, applying only new innovations to avoid the embarrassment of being left behind. 」

E The Times. “The outdated people stick to the end. They valued traditional methods of doing things and refused to apply new technologies until they were eliminated by previous systems and forced to do it. 」

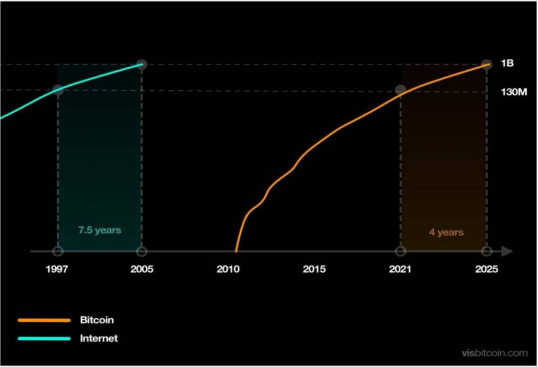

Bitcoin has captured the human imagination. Bitcoin’s story is perhaps more tempting than any previous high-tech innovation. It brings the most cutting-edge innovation to one of the foundations of mankind: currency. Given the possibility of revolutionizing such a fundamental concept, Bitcoin underwent several speculative cycles in its brief history. However, it would be a serious mistake to use these cycles as grounds for denying Bitcoin. These cycles are a well-understood psychological phenomenon caused by man’s fascination with new things. Moreover, any excessive emphasis on foam is to see the trees without the forest. Because, in just 12 years, Bitcoin has grown to 135 million users worldwide, with a faster application rate than the Internet, mobile phone, or virtual banking tools, namely PayPal, in the comparable period. At the current application rate, Bitcoin will reach 1 billion users in four years. Bitcoin, like all previous innovative technologies, is following a predictable and transparent application curve, although accelerating.

Such an incremental user base, the dividend period retained to us ordinary people about how long still?

Which track should we choose during the dividend period, and what can we can and do on this track?

These will be left for everyone to sink down to think;

For me personally, why I choose quantitative trading this derivative as a long-term development track, why I choose ACI quantitative robot, below I explain this question from two aspects.

First, the above mentioned Bitcoin development rate and user growth base, then for this market must be more and more user growth base, because this is the market of mankind, is Bitcoin’s original design concept —— decentralization, in the future, more and more people will enter the huge market derived from the digital currency such as bitcoin, Ethereum; the longer time period, one year, two years or five years, this cycle youcan grasp the number of your wealth appreciation (the biggest wealth);

Second, the first thing new users enter the market must face the secondary market, retained in the secondary market will learn currency speculation and trading, so what is the biggest difference between quantitative and labor? To enter the secondary market to do trading, the first is to learn mathematics, physics and chemistry, the second is anti-humanity, to face and accept the market of every market fluctuations, the third is to establish a set of their own trading system and resolutely implement. These three points seem simple, but need the hard conditions: 1, talent; 2, systematic learning and combat; 3,5 or even over 10 years of full-time experience; otherwise why there has been a saying: one profit, two draws, two losses and seven losses. Ask, if every user can make money in the digital money market, where does the money come from? And quantitative trading it is more suitable for ordinary players, it also has a scientific name called algorithm trading, it will replace artificial strategy, with mathematical models and scientific strategy, to achieve a certain conditions, but its profit is a stable long-term absolute value, rather than the short term of wealth; because each of us enter the digital currency secondary market, the original intention is to improve life, achieve wealth growth, increase the happiness index;

Third, why do you choose the ACI quantitative robot as a tool to fry the currency?

1. Select any product to make a comparison, especially the financial industry; here put forward a core: withdrawal rate is linked to risk, and the secondary market price of digital currency fluctuates greatly, a careless will be a large withdrawal, so we choose the product is not its return rate, but two products, product recovery rate is 100%, and 50%, product 20 year rate is 70%, and the withdrawal rate is 10%, the choice is only product 2;

2. Fund utilization rate, not just play finance, as long as you do business you will understand that the nature of business is not related to fund utilization, the greater your capital utilization proves that the more you can do, the more pipeline to profit; (those who play Martin strategy)

3. The concept reflected by the ACI quantitative robot is also consistent with the personal development ideal, It is free and continuously updated and optimized for life, Of course there is no free lunch, After all, everything takes costs, It charges a small transaction fee, To mark 99.99% of the various products on the current market, All exceptions are the lowest 20% profit withdrawals, Take an example here, If 10,000 u profit 1,000 u, Excluding withdrawal servants and exchange fees, Only over 700 u, came up with While the same ACI quantized robot profits 1,000 u, with 10,000 u Remove fees, Final hand 935-940u;

4. API technology interface of trading platform, do quantitative is a core is security and stability, as the three head compliance trading platform —— currency network, I think I don’t need me to introduce, whether from the user base, trading depth or technical security, is the best choice, after all, security and stability is not what we want;

Simply summary, quantification is actually statistics

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Press Release

SEER Robotics Reports Over 460 Percent Year-over-Year Growth in Overseas New Orders in the First Five Months of 2026

Overseas customer base grows significantly as the company expands its global market presence

Shanghai, China, 11th Aug 2026, Grand Newswire – SEER Robotics, a platform-based embodied intelligent robotics company, today announced strong growth in its overseas business during the first five months of 2026. From January to May 2026, the company’s new overseas orders increased by more than 460% year-over-year, while its overseas customer base expanded significantly during the same period.

The results reflect increasing global adoption of intelligent robotics technologies as industrial customers seek scalable and reliable automation capabilities.

SEER Robotics focuses on intelligent robot control systems, which the company refers to as the “robot brain.” The company develops robot controllers, software platforms, robots and related components, supporting the development, deployment and operation of robotic systems across industrial sectors.

According to China Insights Consultancy (CIC), an industry research firm, SEER Robotics ranked first globally in intelligent robot controller shipments for three consecutive years from 2023 to 2025. In 2025, the company’s global market share in intelligent robot controllers reached 24.8%, while its market share in China reached 45.2%. During the same period, SEER Robotics’ ranking in global industrial intelligent robot shipments improved from third place in 2024 to second place in 2025.

Previously disclosed financial information shows that SEER Robotics’ revenue increased from RMB 249 million in 2023 to RMB 442 million in 2025, representing a three-year compound annual growth rate (CAGR) of 33.2%. The company’s overall gross margin reached 47.4% in 2025, while its core controller business has consistently maintained gross margins above 80%.

According to the company, robots powered by SEER Robotics’ control systems have accumulated more than 60 million hours of operation across different robot platforms and application scenarios. As of August 2026, the SEER Robotics platform supports more than 2,000 robot models, is compatible with more than 400 core components, serves more than 2,100 customers worldwide, and supports applications across more than 35 countries and regions.

SEER Robotics was listed on the Main Board of the Hong Kong Stock Exchange on June 24, 2026, becoming the first Hong Kong-listed company focused on the “robot brain.” The company raised approximately HK$1.226 billion through its initial public offering, including the exercise of the over-allotment option.

About SEER Robotics

SEER Robotics is a platform-based embodied intelligent robotics company, with core businesses spanning robot controllers, AMRs, and embodied intelligent robots. Built on its “robot brain” technology, SEER Robotics provides 1,000+ intelligent robot solutions worldwide and has built an open robotics platform for large-scale deployment.

Media Contact

Organization: SEER Robotics

Contact

Person: Ruby

Website:

https://seer-robotics.ai/

Email:

contact@seer-robotics.ai

Address:Building 3, No. 799, Dangui Road, Pudong New Area, Shanghai 201318

City: Shanghai

Country:China

The post SEER Robotics Reports Over 460 Percent Year-over-Year Growth in Overseas New Orders in the First Five Months of 2026

appeared first on Grand Newswire.

It is provided by a third-party content provider. Grand Newswire makes no

warranties or representations in connection with it.

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Press Release

ForumPay Expands Payment Infrastructure with New Card and Bank Transfer Acceptance Solution

Milton, Georgia, August 11th, 2026, Chainwire

Businesses are increasingly looking for ways to offer more payment options without adding operational complexity. ForumPay, a crypto payment infrastructure company, enables merchants to accept crypto payments across online, in-store, and in-app channels, with instant conversion and next-day settlement.

ForumPay has recently announced a new payment flow that it says could meaningfully alter how payments are processed. Customers can now initiate purchases using any Visa or Mastercard and bank transfers in selected markets, with funds routed automatically through ForumPay’s infrastructure. Merchants can now offer card and bank payments without registering as a card acceptance businesses, sidestepping chargeback liability and PCI-DSS compliance costs while still receiving precisely the amount invoiced.

This latest ForumPay release represents one of the more ambitious developments yet to bridge the gap between traditional payment rails and crypto infrastructure.

Built for Modern Payment Acceptance

Businesses increasingly want to offer customers greater flexibility at checkout, but additional payment methods tend to bring additional operational and cost burdens. Card acceptance, in particular, can introduce chargeback exposure, compliance requirements, fraud management responsibilities, and more complex settlement processes, challenges that only grow more acute for organizations operating across multiple markets.

ForumPay’s innovative new payment flow is designed to solve these issues. Customers can initiate payments using any Visa, Mastercard, or bank transfer in selected markets, with those funds automatically used to purchase crypto and processed through ForumPay’s existing crypto payment infrastructure, with all of the inherent features and benefits, and converted and settled as per the preferences a merchant has already established on their account. Merchants will receive exactly the amount invoiced. For example, if a customer is billed $100, then $100 is what arrives in the merchant’s preferred bank account.

Critically, ForumPay will pass the additional card and bank transfer costs directly to the payer, meaning merchants pay only their usual crypto acceptance fees that would apply to any transaction processed through the platform. The approach allows businesses to expand the choice of available payment methods at checkout without taking on the compliance architecture, risks and costs that card acceptance would ordinarily require.

More Payment Options, the Same Operational Footprint

Businesses increasingly want to offer customers greater flexibility at checkout, but incorporating additional payment methods tend to bring with it additional operational burdens. Card acceptance, in particular, can introduce chargeback exposure, compliance requirements, fraud management responsibilities, and more complex settlement processes, challenges that only grow more acute for organizations operating across multiple markets.

ForumPay’s new payment flow is being designed to address this friction. Customers will be able to initiate payments using any Visa, Mastercard, or bank transfer in selected markets. Those funds are then automatically used to purchase digital assets and processed through ForumPay’s existing infrastructure, allowing merchants to continue receiving funds according to their established settlement preferences without having to overhaul their operations to accommodate the new options in the process. The approach, ForumPay says, allows businesses to expand what they can offer at checkout without taking on the compliance architecture that card acceptance would ordinarily require.

About ForumPay

ForumPay is a complete cryptocurrency-to-fiat payment technology firm; its core processing technology helps businesses attract new customers, optimize customers’ ability to spend, and increase revenue. ForumPay’s wallet-agnostic solution enables crypto consumers to spend their preferred cryptocurrency, from any wallet for everyday goods and services to luxury goods, automobiles, real estate, and private jets. ForumPay eliminates merchant exposure or risk by processing transactions with instant crypto-to-cash conversion. ForumPay merchants receive payments in the currency of their choice directly into their bank account. The transactional experience is similar to accepting other popular payment methods, including cash, credit cards, and bank transfers, but simpler, faster, and more secure.

Contact

Director Global Account Management

Paul Wordsworth

ForumPay

paul@forumpay.com

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Naples, FL, USA, August 11th, 2026, FinanceWire

Drones have become a growing security problem, and the market to stop them is expanding just as quickly. MarketsandMarkets estimates the global counter-unmanned aircraft systems market will grow from $6.64 billion in 2025 to $20.31 billion by 2030, representing a 25.1 percent compound annual growth rate. Within that forecast, AI-powered counter-UAS is the fastest-growing technology layer, projected to expand from $0.9 billion in 2025 to $6.2 billion by 2030. As governments and critical infrastructure operators look for ways to detect, track, and defeat increasingly sophisticated drone threats, defense companies are racing to build the next generation of counter-UAS technology. Several public companies are already staking positions in counter-UAS, approaching the opportunity from different angles.

Change Agents Corp. (Nasdaq: CHGA) has joined the Institute for Defense and Government Advancement, or IDGA, and will take part in the organization’s Counter UAS Summit. Now in its eighth year, the summit runs August 25 to 26 at the MGM National Harbor in Maryland under the chairmanship of retired General Glen VanHerck, former commander of North American Aerospace Defense Command and U.S. Northern Command. IDGA expects more than 500 senior decision-makers, acquisition leaders, and program managers from the Army, Navy, Air Force, Marines, Customs and Border Protection, and law enforcement, placing Change Agents in direct contact with the buyers and technology developers shaping counter-drone procurement.

The summit role builds on the company’s August 4 launch of Autonomous Air Defense LLC, a wholly owned subsidiary formed to identify, evaluate, acquire, and develop autonomous air defense and counter-UAS technologies. That announcement also brought retired Major General Malcolm Frost onto the advisory boards of both Change Agents and the new subsidiary. Frost served 31 years in the U.S. Army, retiring as a two-star general after commanding the 2nd Stryker Brigade Combat Team of the 25th Infantry Division and serving as Deputy Commanding General of the 82nd Airborne Division. He is a West Point and Army War College graduate who deployed to Bosnia, Iraq, and Afghanistan, and he advises public and private companies across the defense and technology sectors.

Change Agents built its business in agentic AI software, pairing an AI search optimization platform called Beacon with an autonomous content creation platform called Catch-Up, both sold on a subscription model. Management frames the counter-drone move as an outgrowth of that work rather than a break from it. Director Michael Mathews called the formation of Autonomous Air Defense LLC “a natural extension of the company’s broader artificial intelligence strategy” and tied the IDGA engagement to positioning the company to “capitalize on the significant long-term opportunities within the global counter-UAS market. ” Frost, in joining, pointed to the convergence of artificial intelligence, autonomous systems, and next-generation counter-drone technology as one of the most important developments in modern defense.

That convergence is the opening Change Agents intends to pursue, and the sequence so far has been deliberate. In roughly a week the company has stood up a dedicated subsidiary, added a decorated defense advisor, and secured a place at the sector’s principal U.S. gathering. The company has said Autonomous Air Defense is evaluating multiple acquisition and partnership opportunities involving AI-enabled counter-drone technologies serving defense, homeland security, and critical infrastructure customers, and that it expects to provide further updates as developments occur.

Change Agents is entering a field already populated by well-funded public companies attacking the drone problem from different angles.

Ondas Inc. (Nasdaq: ONDS) is the closest analog to what Change Agents describes. Its Iron Drone Raider is an autonomous net-based interceptor built to neutralize hostile drones without jamming, paired with its Sentrycs platform for cyber and radio-frequency detection and identification, together mirroring the detect, identify, track, and intercept sequence Change Agents has said it wants to reach. Ondas posted first-quarter 2026 revenue of $50.1 million against a pro forma backlog of $457 million and in July raised its full-year 2026 revenue target to at least $525 million. In February its Airobotics subsidiary secured a multi-million-dollar order from a European customer in a NATO country following an Iron Drone Raider deployment at a major international airport, one of the few operational uses of an interceptor drone in a live civil-aviation setting.

AeroVironment (Nasdaq: AVAV) approaches the market as an established contractor. Its acquisition of BlueHalo, valued at roughly $4.1 billion and completed in May 2025, added directed energy, electronic warfare, and counter-UAS capabilities to a portfolio already known for the Switchblade family of loitering munitions. BlueHalo had delivered its 1,000th Titan radio-frequency counter-UAS system before the deal closed and was the first to operationally field a laser weapon system with LOCUST. The combination turned a former drone specialist into a diversified defense technology platform spanning radio-frequency, directed energy, and kinetic defeat, and it marks the scaled version of the category Change Agents is entering.

Kratos Defense & Security Solutions (Nasdaq: KTOS) anchors the autonomous systems end of the field. Best known for the jet-powered XQ-58A Valkyrie, Kratos reported second-quarter 2026 revenue of $458.8 million, up 30.5 percent year over year and 19.1 percent organically, and raised full-year 2026 guidance to a range of $1.75 billion to $1.81 billion. Total backlog stood at $2.084 billion against a bid pipeline of $15.0 billion, a measure of how much defense money is now moving through unmanned and autonomous programs, and of the budgets, Change Agents is positioning to reach.

Ondas, AeroVironment, and Kratos map the opportunity from interceptor specialist to diversified prime, and they mark out the market Change Agents Corp. (Nasdaq: CHGA) has chosen to enter. What CHGA has established is a subsidiary, an advisor with two-star command experience, and access to the procurement community setting counter-drone requirements. What remains prospective is the technology itself, and the company has said it expects to report further developments as it works through the acquisition and partnership opportunities in front of it.

Disclaimers: RazorPitch Inc. “RazorPitch” is not operated by a licensed broker, a dealer, or a registered investment adviser. This content is for informational purposes only and is not intended to be investment advice. The Private Securities Litigation Reform Act of 1995 provides investors a safe harbor in regard to forward-looking statements. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, goals, assumptions, or future events or performances are not statements of historical fact and may be forward-looking statements. Forward-looking statements are based on expectations, estimates, and projections at the time the statements are made that involve a number of risks and uncertainties that could cause actual results or events to differ materially from those presently anticipated. Forward-looking statements in this action may be identified through the use of words such as projects, foresee, expects, will, anticipates, estimates, believes, understands, or that by statements indicating certain actions & quote; may, could, or might occur. Understand there is no guarantee past performance will be indicative of future results. Investing in micro-cap and growth securities is highly speculative and carries an extremely high degree of risk. It is possible that an investor’s investment may be lost or impaired due to the speculative nature of the companies profiled. RazorPitch has been retained and compensated by Change Agents Corp to assist in the production and distribution of content related to CHGA. RazorPitch is responsible for the production and distribution of this content. It should be expressly understood that under no circumstances does any information published herein represent a recommendation to buy or sell a security. This content is for informational purposes only; you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by RazorPitch or any third-party service provider to buy or sell any securities or other financial instruments. All content in this article is information of a general nature and does not address the circumstances of any particular individual or entity. Nothing in this article constitutes professional and/or financial advice, nor does any information in the article constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. RazorPitch is not a fiduciary by virtue of any persons use of or access to this content.

Contact

Mark McKelvie

RazorPitch

mark@razorpitch.com

585-301-7700

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

SEER Robotics Reports Over 460 Percent Year-over-Year Growth in Overseas New Orders in the First Five Months of 2026

ForumPay Expands Payment Infrastructure with New Card and Bank Transfer Acceptance Solution

Counter-UAS Market Set to Triple by 2030 as Defense Companies Position for Growth

Benzinga Money Article Discusses How to Become Part of the 12% of Retirees Who Have Achieved the Recommended $550,000 Minimum Retirement Savings Threshold

Apu Apustaja Conquers New York with Lively Street Ads, Including Times Square Billboard

Bay Smokes Maintains Quality Amid Legislative Changes in the Hemp Industry

-

Press Release4 days ago

STARTRADER in Discussions with Trustpilot to Consolidate Review Profiles

-

Press Release15 hours ago

Demeter Tactical Investments (ME) Limited bolsters governance with two board appointments

-

Press Release5 hours ago

ForumPay Expands Payment Infrastructure with New Card and Bank Transfer Acceptance Solution

-

Press Release4 days ago

Fire Safety Innovation in the Spotlight as Industry Expert Paul Trew Speaks Out on Evolving Fire Risk

-

Press Release8 hours ago

Vincere Portfolios Expands Industry Discussion Around the Gap Between Retail Investing Tools and Institutional Trading Infrastructure

-

Press Release4 days ago

Social Security Adjustments Have Failed to Keep Pace with Inflation—How Retirees Can Supplement Their Income Through Bitcoin Mining in 2026

-

Press Release6 days ago

Global Hit Anime Jaadugar: A Witch in Mongolia Unveils 3rd Main PV and Visual, Kujira as 1st Empress

-

Press Release6 days ago

From a Free Book to a Business in the Making: Entrepreneur Vanessa Murphy Launches Trading My Way Barter Journey Across the U.S.