Press Release

A New Horizon on Financial Future: Trister World’s New Ecology of DeFi Financial Aggregation

Today, Defi locked in over $40 billion of assets, a nibble of share, compared to the market cap of crypto assets $1.2 or so trillion. In traditional finance, the traditional derivatives market is worth hundreds of trillions of dollars, and the crypto market as a whole is less than 0.1% of its asset size, even the combined wealth of the people at the top of the pyramid is five or more times larger than total assets of the entire crypto market.

Yet this is an opportunity for DeFi to grow.

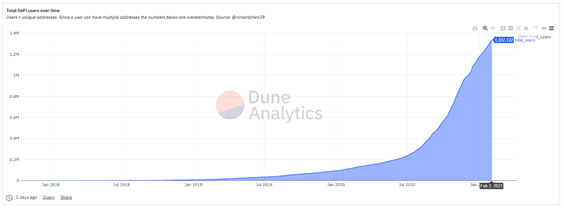

According to statistics, the total number of DeFi users has outpaced 1 million. Among them, the figure for Uniswap users soared to 586,000, taking the crown on the list with 58.6%, followed by Compound with 254,000, Kyber 110,000, 1inch 43,000 and OpenSea 33,000, respectively.

(Total DeFi users over time)

Decentralised Finance (DeFi for short), a smart contract and protocol for crypto-assets and finance based on the smart contract platform, is dedicated to reengineering the current financial system, creating a transparent system that opens up the application ecosystem to everyone without the need for permission and without relying on the third party to cater to their financial needs. On the eve of a boom, the sector needs a DeFi resource aggregation platform, involving and engaging both regular and experienced users. Not only does it make easier for users to play a part in DeFi, but it dispels their misgivings, be it complex operations, harsh terms, yield guaranty, safety and security or level playing field, among other issues. The sector sees an avalanche of DeFi projects, with fragmented information, difficult judgment of truth and falseness and a high bar. The planning of the total ecological product of DeFi the Trister team recently released is beyond expectation and perception of everyone, its pattern and innovation in particular. Let’s check out what highlights and innovations awoke the public.

Trister World typifies a DeFi resource aggregation platform, featuring “value creation, value circulation and value drive”, built by a team of top crypto scientists in worldwide efforts. On the back of the global community of Trister, Trister World has turned out to be a brand new DeFi ecosystem, with a focus on a new generation of the decentralized financial world for the future. That being said, the new system simplifies as much as possible the complex operations of the users, leaving it to the Trister’s bottom, while the user interface (UI) continues to build a financial inclusion platform, regardless of nation, region, race and wealth, a boon to the users. Users in yield farming, for instance, may enjoy lower costs, fewer operations, faster speed and higher returns.

The yellow paper on Trister World’s technical development plan the Trister team published recently explicitly elucidates that, upon reaching three major milestones, Trister comes to Trister World, an upgrading of the strategy. The continued updates and iterations enabled more DeFi enthusiasts to know, understand and take part in the universally-recognised ecosystem.

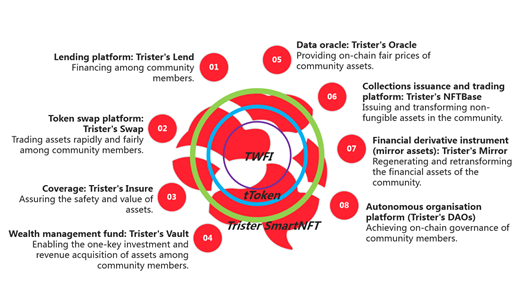

Far cry from other functional DeFi projects, Trister World is not contented with being an “upgrade” or a “substitute” for traditional financial instruments. Rather, it constantly delves into the cutting-edge technologies of the industry across the globe in the creation of a complete aggregation platform. It progressively implements and aggregates a matrix of eight major products, namely Trister’s Lend, Trister’s Swap, Trister’s Vault, Trister’s Insure, Trister’s Oracle, Trister’s NFTBase, Trister’s Mirror and Trister’s DAOs.

(Trister World’s eight major products matrix)

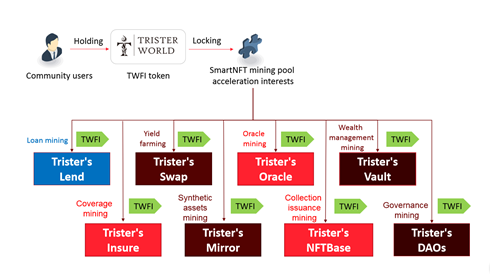

It is understood that Trister World, in possession of three core subjects, is applied to achieving on-chain governance of community members. TWFI, above all, is the core value token of Trister World, bearing with Trister World’s ecological value as well as community governance rights. The total amount in circulation stands at 80 million, with 10 million deployed in each of eight products.

tToken serves as a credential of financial equity for the applications of varied ecological products throughout the entire Trister World. Holding tToken means interest earnings. tToken is synonymous with a key to interoperability between Trister World’s ecologies. Also, holding tToken allows mining in different ecological projects at the same time in an endeavour to make more profits.

Furthermore, Trister SmartNFT(tCard), Trister World’s ecology privilege card, will become the first community NFT asset in the future, the ownership of which is bound to secure a collection of special rights and benefits in all major ecologies.

(Mining logic of Trister World)

Trister World’s new DeFi ecosystem stands out with two salient advantages. First, tToken makes sure interoperability between ecologies while mining in different projects, to generate more revenues. Second, the addition of buyback-destruction-deflation mechanism earmarks 20% of profits for buyback and destruction of TWFI tokens, adding a magic allure to the engagement of users.

Trister World’s initiative, an awe-inspiring innovation, comes forth the implementation and aggregation of eight eco-products in the entire DeFi ecosystem, the first technology of this kind, with a far-reaching ripple to the existing ecosystem, the DeFi ecosystem to be specific. The series of financial products will be interlocked through a combination of functions, and the smart contracts will call each other to connect some financial functions together, building “an ecological economy and a convergence platform”.

It is reported that Trister’s Lend, which will be released in the second quarter, has made a major innovation in its development, allowing institutional users to establish new loan transaction pairs by pledging assets as a way to provide lending services in low liquidity currencies.

(Trister World’s Official twitter)

Never will the journey of Trister World be smooth in the future with brambles and thorns coming along. It will reshape the entire world’s value interaction model and create a new pattern of DeFi ecology should it be carried on. We look forward to the launch of Trister’s Lend and keep you abreast of the up-to-minute progress of Trister World.

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Press Release

ForumPay Expands Payment Infrastructure with New Card and Bank Transfer Acceptance Solution

Milton, Georgia, August 11th, 2026, Chainwire

Businesses are increasingly looking for ways to offer more payment options without adding operational complexity. ForumPay, a crypto payment infrastructure company, enables merchants to accept crypto payments across online, in-store, and in-app channels, with instant conversion and next-day settlement.

ForumPay has recently announced a new payment flow that it says could meaningfully alter how payments are processed. Customers can now initiate purchases using any Visa or Mastercard and bank transfers in selected markets, with funds routed automatically through ForumPay’s infrastructure. Merchants can now offer card and bank payments without registering as a card acceptance businesses, sidestepping chargeback liability and PCI-DSS compliance costs while still receiving precisely the amount invoiced.

This latest ForumPay release represents one of the more ambitious developments yet to bridge the gap between traditional payment rails and crypto infrastructure.

Built for Modern Payment Acceptance

Businesses increasingly want to offer customers greater flexibility at checkout, but additional payment methods tend to bring additional operational and cost burdens. Card acceptance, in particular, can introduce chargeback exposure, compliance requirements, fraud management responsibilities, and more complex settlement processes, challenges that only grow more acute for organizations operating across multiple markets.

ForumPay’s innovative new payment flow is designed to solve these issues. Customers can initiate payments using any Visa, Mastercard, or bank transfer in selected markets, with those funds automatically used to purchase crypto and processed through ForumPay’s existing crypto payment infrastructure, with all of the inherent features and benefits, and converted and settled as per the preferences a merchant has already established on their account. Merchants will receive exactly the amount invoiced. For example, if a customer is billed $100, then $100 is what arrives in the merchant’s preferred bank account.

Critically, ForumPay will pass the additional card and bank transfer costs directly to the payer, meaning merchants pay only their usual crypto acceptance fees that would apply to any transaction processed through the platform. The approach allows businesses to expand the choice of available payment methods at checkout without taking on the compliance architecture, risks and costs that card acceptance would ordinarily require.

More Payment Options, the Same Operational Footprint

Businesses increasingly want to offer customers greater flexibility at checkout, but incorporating additional payment methods tend to bring with it additional operational burdens. Card acceptance, in particular, can introduce chargeback exposure, compliance requirements, fraud management responsibilities, and more complex settlement processes, challenges that only grow more acute for organizations operating across multiple markets.

ForumPay’s new payment flow is being designed to address this friction. Customers will be able to initiate payments using any Visa, Mastercard, or bank transfer in selected markets. Those funds are then automatically used to purchase digital assets and processed through ForumPay’s existing infrastructure, allowing merchants to continue receiving funds according to their established settlement preferences without having to overhaul their operations to accommodate the new options in the process. The approach, ForumPay says, allows businesses to expand what they can offer at checkout without taking on the compliance architecture that card acceptance would ordinarily require.

About ForumPay

ForumPay is a complete cryptocurrency-to-fiat payment technology firm; its core processing technology helps businesses attract new customers, optimize customers’ ability to spend, and increase revenue. ForumPay’s wallet-agnostic solution enables crypto consumers to spend their preferred cryptocurrency, from any wallet for everyday goods and services to luxury goods, automobiles, real estate, and private jets. ForumPay eliminates merchant exposure or risk by processing transactions with instant crypto-to-cash conversion. ForumPay merchants receive payments in the currency of their choice directly into their bank account. The transactional experience is similar to accepting other popular payment methods, including cash, credit cards, and bank transfers, but simpler, faster, and more secure.

Contact

Director Global Account Management

Paul Wordsworth

ForumPay

paul@forumpay.com

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

Naples, FL, USA, August 11th, 2026, FinanceWire

Drones have become a growing security problem, and the market to stop them is expanding just as quickly. MarketsandMarkets estimates the global counter-unmanned aircraft systems market will grow from $6.64 billion in 2025 to $20.31 billion by 2030, representing a 25.1 percent compound annual growth rate. Within that forecast, AI-powered counter-UAS is the fastest-growing technology layer, projected to expand from $0.9 billion in 2025 to $6.2 billion by 2030. As governments and critical infrastructure operators look for ways to detect, track, and defeat increasingly sophisticated drone threats, defense companies are racing to build the next generation of counter-UAS technology. Several public companies are already staking positions in counter-UAS, approaching the opportunity from different angles.

Change Agents Corp. (Nasdaq: CHGA) has joined the Institute for Defense and Government Advancement, or IDGA, and will take part in the organization’s Counter UAS Summit. Now in its eighth year, the summit runs August 25 to 26 at the MGM National Harbor in Maryland under the chairmanship of retired General Glen VanHerck, former commander of North American Aerospace Defense Command and U.S. Northern Command. IDGA expects more than 500 senior decision-makers, acquisition leaders, and program managers from the Army, Navy, Air Force, Marines, Customs and Border Protection, and law enforcement, placing Change Agents in direct contact with the buyers and technology developers shaping counter-drone procurement.

The summit role builds on the company’s August 4 launch of Autonomous Air Defense LLC, a wholly owned subsidiary formed to identify, evaluate, acquire, and develop autonomous air defense and counter-UAS technologies. That announcement also brought retired Major General Malcolm Frost onto the advisory boards of both Change Agents and the new subsidiary. Frost served 31 years in the U.S. Army, retiring as a two-star general after commanding the 2nd Stryker Brigade Combat Team of the 25th Infantry Division and serving as Deputy Commanding General of the 82nd Airborne Division. He is a West Point and Army War College graduate who deployed to Bosnia, Iraq, and Afghanistan, and he advises public and private companies across the defense and technology sectors.

Change Agents built its business in agentic AI software, pairing an AI search optimization platform called Beacon with an autonomous content creation platform called Catch-Up, both sold on a subscription model. Management frames the counter-drone move as an outgrowth of that work rather than a break from it. Director Michael Mathews called the formation of Autonomous Air Defense LLC “a natural extension of the company’s broader artificial intelligence strategy” and tied the IDGA engagement to positioning the company to “capitalize on the significant long-term opportunities within the global counter-UAS market. ” Frost, in joining, pointed to the convergence of artificial intelligence, autonomous systems, and next-generation counter-drone technology as one of the most important developments in modern defense.

That convergence is the opening Change Agents intends to pursue, and the sequence so far has been deliberate. In roughly a week the company has stood up a dedicated subsidiary, added a decorated defense advisor, and secured a place at the sector’s principal U.S. gathering. The company has said Autonomous Air Defense is evaluating multiple acquisition and partnership opportunities involving AI-enabled counter-drone technologies serving defense, homeland security, and critical infrastructure customers, and that it expects to provide further updates as developments occur.

Change Agents is entering a field already populated by well-funded public companies attacking the drone problem from different angles.

Ondas Inc. (Nasdaq: ONDS) is the closest analog to what Change Agents describes. Its Iron Drone Raider is an autonomous net-based interceptor built to neutralize hostile drones without jamming, paired with its Sentrycs platform for cyber and radio-frequency detection and identification, together mirroring the detect, identify, track, and intercept sequence Change Agents has said it wants to reach. Ondas posted first-quarter 2026 revenue of $50.1 million against a pro forma backlog of $457 million and in July raised its full-year 2026 revenue target to at least $525 million. In February its Airobotics subsidiary secured a multi-million-dollar order from a European customer in a NATO country following an Iron Drone Raider deployment at a major international airport, one of the few operational uses of an interceptor drone in a live civil-aviation setting.

AeroVironment (Nasdaq: AVAV) approaches the market as an established contractor. Its acquisition of BlueHalo, valued at roughly $4.1 billion and completed in May 2025, added directed energy, electronic warfare, and counter-UAS capabilities to a portfolio already known for the Switchblade family of loitering munitions. BlueHalo had delivered its 1,000th Titan radio-frequency counter-UAS system before the deal closed and was the first to operationally field a laser weapon system with LOCUST. The combination turned a former drone specialist into a diversified defense technology platform spanning radio-frequency, directed energy, and kinetic defeat, and it marks the scaled version of the category Change Agents is entering.

Kratos Defense & Security Solutions (Nasdaq: KTOS) anchors the autonomous systems end of the field. Best known for the jet-powered XQ-58A Valkyrie, Kratos reported second-quarter 2026 revenue of $458.8 million, up 30.5 percent year over year and 19.1 percent organically, and raised full-year 2026 guidance to a range of $1.75 billion to $1.81 billion. Total backlog stood at $2.084 billion against a bid pipeline of $15.0 billion, a measure of how much defense money is now moving through unmanned and autonomous programs, and of the budgets, Change Agents is positioning to reach.

Ondas, AeroVironment, and Kratos map the opportunity from interceptor specialist to diversified prime, and they mark out the market Change Agents Corp. (Nasdaq: CHGA) has chosen to enter. What CHGA has established is a subsidiary, an advisor with two-star command experience, and access to the procurement community setting counter-drone requirements. What remains prospective is the technology itself, and the company has said it expects to report further developments as it works through the acquisition and partnership opportunities in front of it.

Disclaimers: RazorPitch Inc. “RazorPitch” is not operated by a licensed broker, a dealer, or a registered investment adviser. This content is for informational purposes only and is not intended to be investment advice. The Private Securities Litigation Reform Act of 1995 provides investors a safe harbor in regard to forward-looking statements. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, goals, assumptions, or future events or performances are not statements of historical fact and may be forward-looking statements. Forward-looking statements are based on expectations, estimates, and projections at the time the statements are made that involve a number of risks and uncertainties that could cause actual results or events to differ materially from those presently anticipated. Forward-looking statements in this action may be identified through the use of words such as projects, foresee, expects, will, anticipates, estimates, believes, understands, or that by statements indicating certain actions & quote; may, could, or might occur. Understand there is no guarantee past performance will be indicative of future results. Investing in micro-cap and growth securities is highly speculative and carries an extremely high degree of risk. It is possible that an investor’s investment may be lost or impaired due to the speculative nature of the companies profiled. RazorPitch has been retained and compensated by Change Agents Corp to assist in the production and distribution of content related to CHGA. RazorPitch is responsible for the production and distribution of this content. It should be expressly understood that under no circumstances does any information published herein represent a recommendation to buy or sell a security. This content is for informational purposes only; you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by RazorPitch or any third-party service provider to buy or sell any securities or other financial instruments. All content in this article is information of a general nature and does not address the circumstances of any particular individual or entity. Nothing in this article constitutes professional and/or financial advice, nor does any information in the article constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. RazorPitch is not a fiduciary by virtue of any persons use of or access to this content.

Contact

Mark McKelvie

RazorPitch

mark@razorpitch.com

585-301-7700

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

San Francisco, California, USA, August 11th, 2026, FinanceWire

The ranking validates HoneyBook’s growing reputation as an innovator accelerating the digital transformation of independent businesses globally

HoneyBook, the leading AI-native client relationship platform for small business owners, has been recognized as one of the world’s most significant financial technology firms in CNBC’s 2026 list of the World’s Top Fintech Companies. Its inclusion in the prestigious global list within the Enterprise Fintech category underscores the impact that HoneyBook’s software has had in helping individual business owners to cultivate strong customer relationships.

Produced in partnership with Statista, CNBC’s list is a recognized annual ranking that serves to highlight the world’s most innovative and forward-thinking financial software firms. As part of its assessment process, CNBC evaluates thousands of eligible firms, ranging from startups to established enterprises, based on key performance indicators such as revenue and user growth, transaction volume, business impact and technological innovation. HoneyBook’s debut on this year’s list reflects growing recognition of its platform.

HoneyBook is noted for accelerating automation in the customer relationship management software niche, helping business and freelancers to better manage their day-to-day dealings with clients. Its platform frees users from spending hours on critical business tasks such as capturing and verifying inquiries, drafting proposals, obtaining signatures on contracts, sharing files with customers and processing transactions. With HoneyBook, business owners can manage their administrative and financial operations in a unified platform, making use of autonomous AI agents to perform work they once spent hours on. By linking client communications with financial operations, HoneyBook helps business professionals to work more efficiently and get paid promptly.

CNBC’s recognition of HoneyBook follows the rapid expansion of its client relationship platform into new verticals. Last month, HoneyBook launched a dedicated version of its CRM platform for professional photographers, featuring specialized tools for client bookings, creating schedules, managing their galleries and collaborating with clients on projects. With HoneyBook, photographers get more time to focus on their clients and their work instead of worrying about the administrative side of their business.

“I’m extremely proud that our endeavors to enhance and simplify client relationships have led to HoneyBook being recognized by CNBC as one of the world’s best fintech companies,” said Oz Alon, co-founder and Chief Executive Officer of HoneyBook. “By enabling business owners to nurture relationships with clients in the same place as they manage their finances, HoneyBook significantly reduces the complexity they face when using multiple fragmented tools. CNBC’s recognition validates our ability to empower independent entrepreneurs with innovative tools that streamline the day-to-day aspects of business management.”

About HoneyBook

HoneyBook is the leading AI-powered customer relationship management (CRM) platform for independent business owners, making it easy to sell and deliver their services online. Offering powerful tools for communication, contracts, invoicing, payments and more, the platform puts independent professionals in control of their process and client experience. HoneyBook is trusted by over 100,000 service-based businesses in the United States, Australia, Canada, and the United Kingdom that have booked more than $10 billion in business on the platform. The company has offices in San Francisco and Tel Aviv, with remote staff worldwide. Learn more at HoneyBook.com.

Contact

Dan Edelstein

InboundJunction

pr@inboundjunction.com

About Author

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No Digi Observer journalist was involved in the writing and production of this article.

ForumPay Expands Payment Infrastructure with New Card and Bank Transfer Acceptance Solution

Counter-UAS Market Set to Triple by 2030 as Defense Companies Position for Growth

HoneyBook Included in CNBC’s 2026 List of the World’s Top Fintech Companies

Benzinga Money Article Discusses How to Become Part of the 12% of Retirees Who Have Achieved the Recommended $550,000 Minimum Retirement Savings Threshold

Apu Apustaja Conquers New York with Lively Street Ads, Including Times Square Billboard

Bay Smokes Maintains Quality Amid Legislative Changes in the Hemp Industry

-

Press Release4 days ago

STARTRADER in Discussions with Trustpilot to Consolidate Review Profiles

-

Press Release11 hours ago

Demeter Tactical Investments (ME) Limited bolsters governance with two board appointments

-

Press Release4 days ago

Fire Safety Innovation in the Spotlight as Industry Expert Paul Trew Speaks Out on Evolving Fire Risk

-

Press Release4 days ago

Social Security Adjustments Have Failed to Keep Pace with Inflation—How Retirees Can Supplement Their Income Through Bitcoin Mining in 2026

-

Press Release6 days ago

Global Hit Anime Jaadugar: A Witch in Mongolia Unveils 3rd Main PV and Visual, Kujira as 1st Empress

-

Press Release5 days ago

From a Free Book to a Business in the Making: Entrepreneur Vanessa Murphy Launches Trading My Way Barter Journey Across the U.S.

-

Press Release6 days ago

Borderless.xyz Teams Up with Mastercard to Advance Trusted Cross-Border Stablecoin Payment Flows

-

Press Release4 days ago

Movement, El Vecino and RISE Partner to Launch First Digital Dollar Wallet for Mexican Remittances